Blog

Wishful Thinking, Statistics, and Modeling: Where Could Terramatris Fund Be in September 2026?

| Research | 74 seen

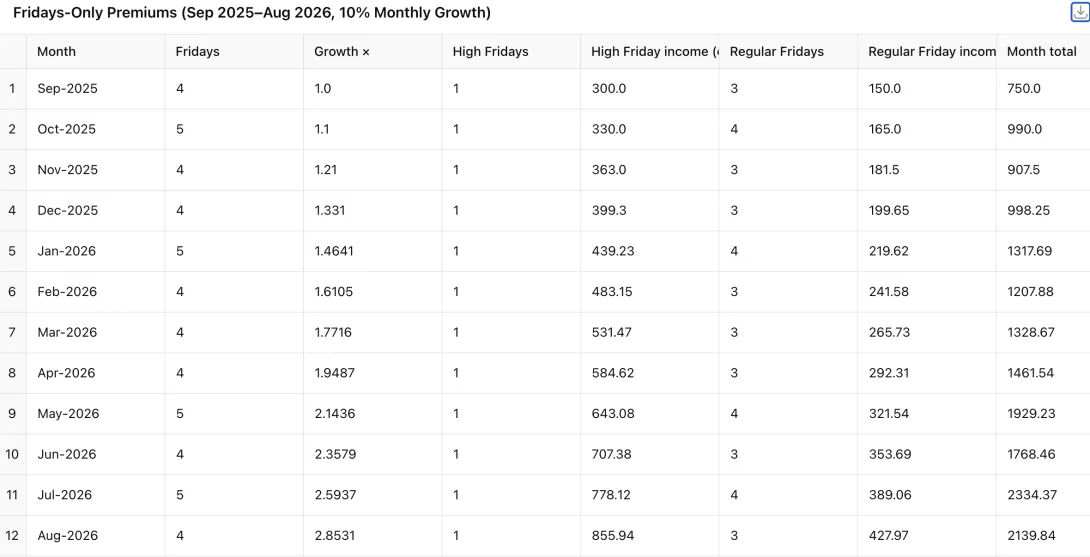

On September 2, 2025, the Terramatris crypto hedge fund stands at $10,500. Out of this, roughly $3,500 is low-interest debt, which we are steadily repaying at a rate of $300–450 per month. If nothing changes, we expect to be debt-free by April 2026. Importantly, there is no real pressure to return these funds quickly; and if market conditions turn against us, we believe we could borrow back on similar terms without risk to the core strategy.

This puts Terramatris in a comfortable position: a five-figure portfolio, a clear debt-repayment path, and a robust options premium strategy that has been delivering consistent weekly returns.

The Options Premium EngineOur core edge comes from selling weekly options—primarily covered calls and short puts.

Base case (regular weeks): $…Trading Covered Calls on XRP with Deribit

| XRP options | 233 seen

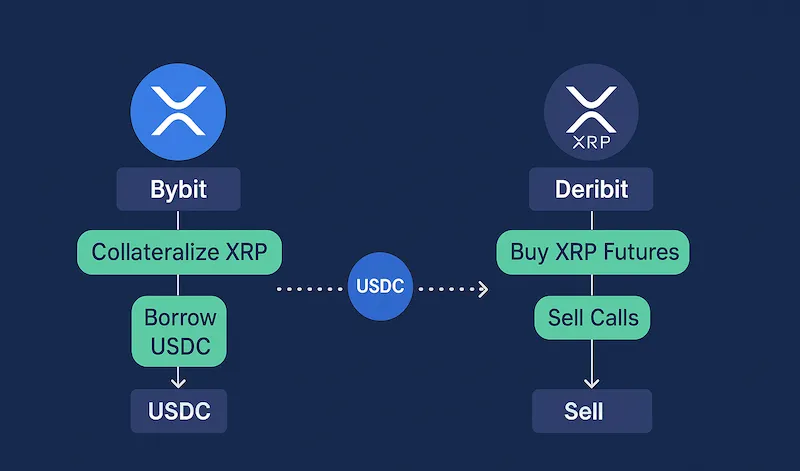

At Terramatris we are always exploring new ways to structure option strategies around crypto assets. One of the more interesting challenges we've faced recently is figuring out how to trade covered calls on XRP.

Covered calls are one of the most popular options income strategies because they allow investors to generate option premium while maintaining long-term exposure to an asset. If you're new to covered calls, start with our guide: How to Generate Income With Ethereum Covered Calls.

While Ethereum options markets are relatively mature, XRP options remain more challenging due to liquidity, settlement, and collateral limitations. This article explores one workaround we tested using Bybit and Deribit.

The Challenge: Collateral Rules on DeribitDeribit lists XRP…

Snipping in DeFi: Tempting, But Not Sustainable

| Research | 68 seen

At Terramatris, we constantly evaluate emerging strategies in the decentralized finance (DeFi) landscape — especially those that promise asymmetric upside. One such tactic is snipping (or sniping), a method that’s gained attention for its high-speed, high-risk approach to token trading.

We want to offer a clear and honest take: while snipping can be entertaining and, in rare cases, wildly profitable, it doesn’t align with our long-term trading philosophy.

What Is Snipping in DeFi?Snipping refers to the practice of purchasing newly launched tokens at the exact moment liquidity is added to decentralized exchanges (DEXs) like Uniswap or Raydium. Traders — typically using bots — aim to front-run others by getting in before a price surge and exiting moments later with a quick…

Selling Covered Calls on Borrowed Bitcoin: Strategic Yield with Asymmetric Risk

| Bitcoin options | 105 seen

On May 25, 2025, we executed a position that perfectly illustrates a niche but compelling setup in the crypto derivatives space. We:

Borrowed 0.01 BTC (worth $1,080 at the time),Posted 0.54 ETH as collateral (worth $1,350),And sold a cash-settled call option on 0.01 BTC with a strike price of $110,000,Collecting a premium of $17 with weekly expiry (May 30).Let’s break down the rationale, benefits, risks, and variations of this strategy — and why, despite its synthetic nature, it can be a valuable tool in Terramatris' option yield strategies.

The Core StrategyThe basic idea is to monetize a borrowed BTC position by selling a cash-settled call option against it. If BTC stays below the strike at expiry, we pocket the premium. If BTC rises above the strike, we owe the…

How to Sell a Synthetic Covered Call on ETH

| Ethereum options | 323 seen

At TerraMatris Crypto Hedge Fund, we actively deploy a range of options strategies to generate income and manage directional exposure. Today, I want to share an elegant and capital-efficient technique we’re using: the synthetic covered call—a method that replicates the payoff profile of a traditional covered call, without the need to hold the underlying crypto asset.

What Is a Synthetic Covered Call?Traditionally, a covered call involves owning a crypto asset (like ETH) and selling a call option against it. This generates premium income while capping upside beyond the strike price. But what if you want to benefit from the same structure without committing capital to the spot position?

The solution is to create a synthetic long position using options and then sell a call…