Blog

Rolling ETH Covered Calls for a 25.35% Potential Return in 42 Days

| Trading Journal | 5 seen

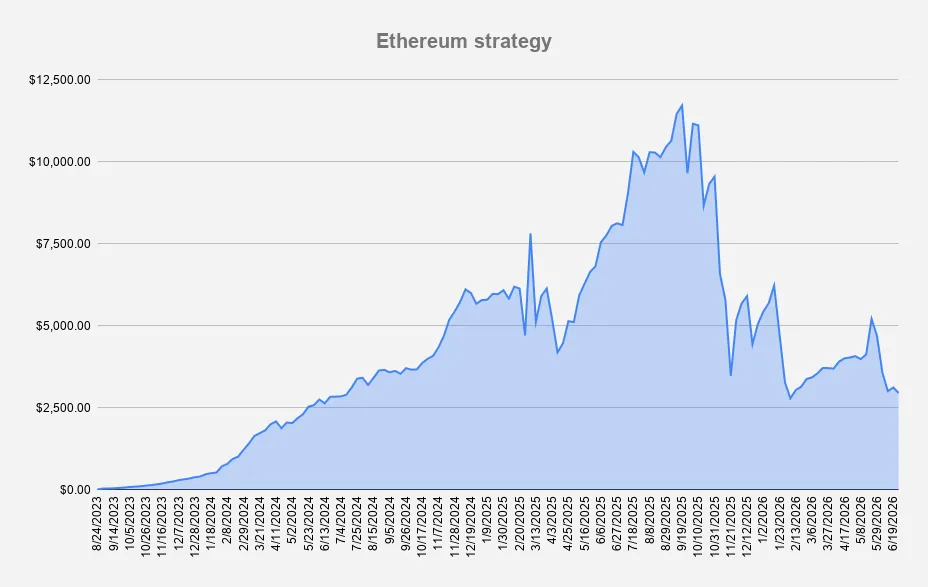

As of July 10, 2026, our Ethereum strategy portfolio was valued at $3,205, up 5.4% week over week. Despite the weekly recovery, the portfolio remains down -40.48% year to date and -72.65% below the all-time high reached in September 2025.

Based on our performance tracking, the strategy is slightly underperforming Ethereum itself, which is down approximately 40.30% year to date.

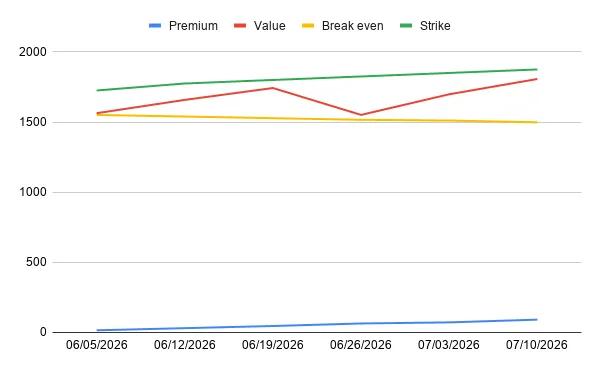

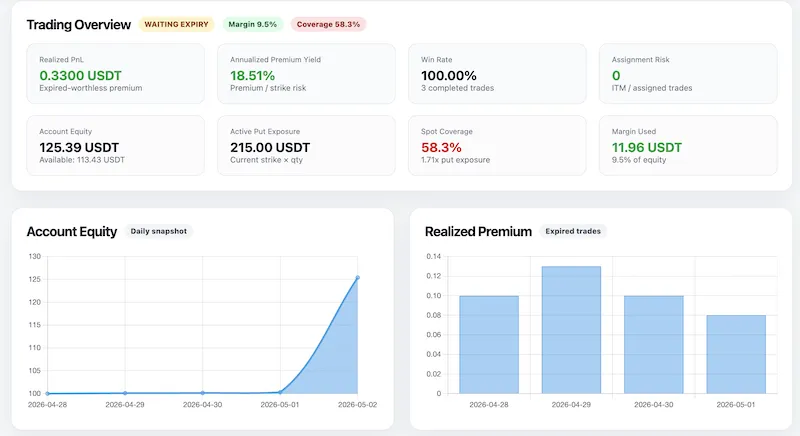

Ethereum Covered Call PositionOn July 7, just a few days before expiry, we decided to roll our 1.3 ETH covered call position up and forward.

We bought back the $1,850 call for $13.40 and sold the July 17 $1,875 call for $29.60. Based on the quoted option prices, the roll generated a gross credit of approximately $16.20 before fees.

According to our portfolio calculations, this increased…

Rolling ETH Covered Calls Toward a 19.02% Return in 35 Days

| Trading Journal | 30 seen

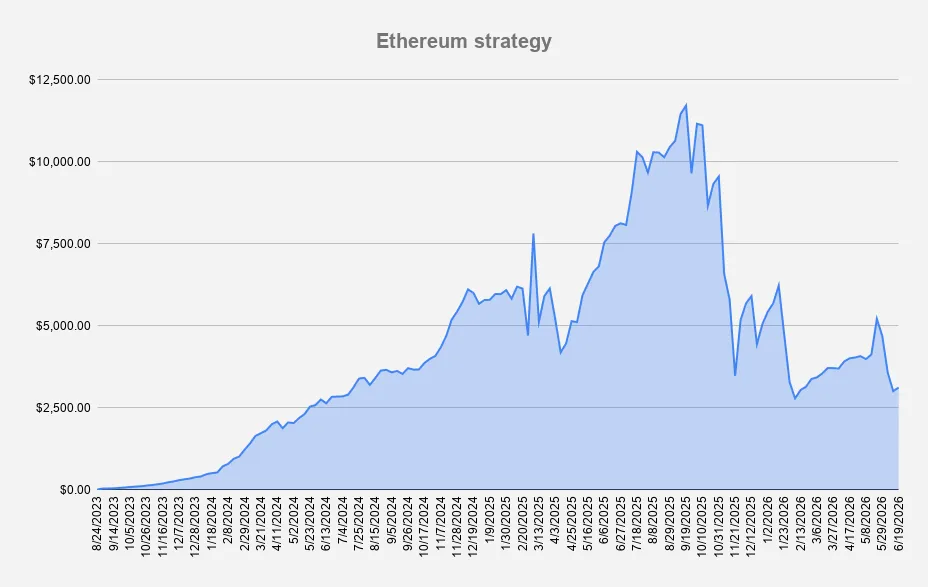

As of July 3, 2026, our Ethereum strategy portfolio was valued at $3,941, up 3.15% week over week. However, the portfolio remains down 43.52% year-to-date and is still significantly below its all-time high, down 74.05% from the record level reached in September 2025.

Our strategy is slightly underperforming Ethereum itself, which is down 42.86% year-to-date.

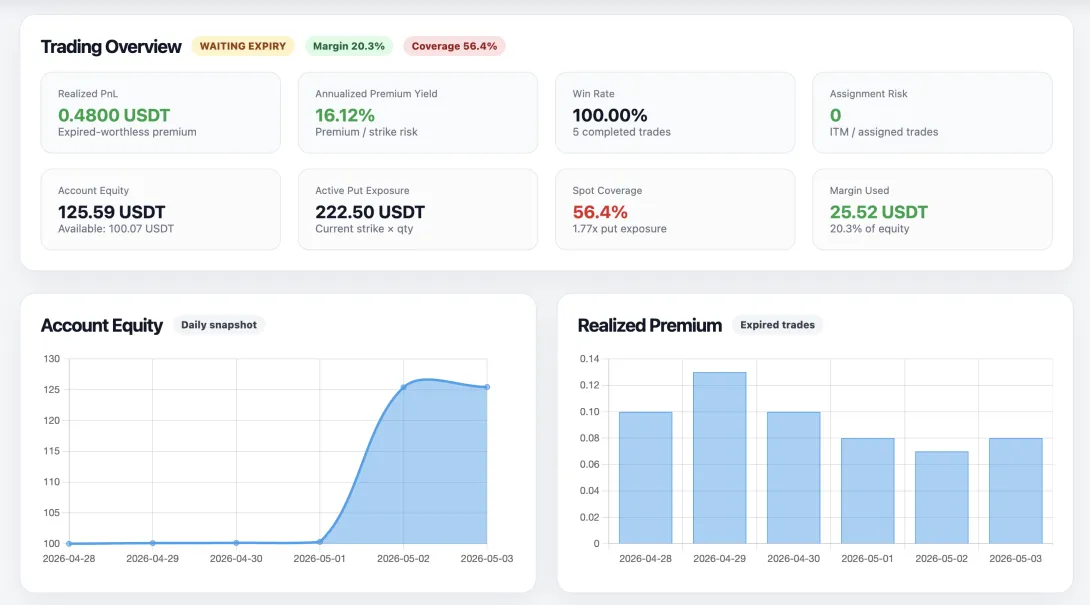

Ethereum Covered Call PositionDuring the week, we rolled our 1.3 ETH position forward and down. One of our weekly options premium goals is to keep the delta below -0.15, and for this week we chose the $1,800 strike.

This roll brought in $7.74, which is barely more than one dollar per day. Still, all premium was reinvested into an ETH spot purchase, increasing our holdings to 1.3045942 ETH.

We now hold:

…Rolling Ethereum Covered Calls for a Potential 20.69% Return in 28 Days

| Trading Journal | 16 seen

As of June 26, 2026, our Ethereum strategy portfolio was valued at $2,948, down 45.25% year-to-date. The recent crypto selloff has been massive - painful, but not exactly unusual for this market.

Compared with Ethereum itself, the portfolio has performed almost identically, with ETH down approximately 48.54% over the same period. In other words, the portfolio has largely tracked its core underlying asset, while still generating option premium along the way.

If there is one lesson to take from this market, it is this: stay away from leverage.

Because we are running spot-only, or spot-backed covered options strategies, we are not being forced out of positions. We are more or less surfing the wave.

During the week, ETH briefly traded above $1,750. At that moment,…

18% Potential Return in 21 Days From Rolling a Single ETH Covered Call

| Trading Journal | 119 seen

As of June 19, 2026, our Ethereum strategy portfolio was valued at $3,116, down 42.15% year-to-date. While that number is never pleasant to see, periods like this are part of investing in both crypto and options.

Rather than chasing risky trades to recover losses quickly, we continue to focus on a disciplined strategy built around generating option premium, managing risk, and gradually lowering our effective cost basis.

Compared with Ethereum itself, the portfolio has performed almost identically, with ETH down approximately 41.54% over the same period. In other words, the portfolio has largely tracked its core underlying asset while continuing to generate option premium along the way.

Ethereum Covered Call PositionThis week, we managed 1.3 Ethereum covered calls…

XRP-Backed ETH Options Strategy: 14.6% Return While Cutting Risk by 80%

| Ethereum options | 38 seen

On April 23, 2026, a smaller XRP-denominated account managed separately from the main Terramatris strategies initiated a structured crypto options income strategy on Bybit.

The account holder approved the strategy specifically to generate additional income from long-term XRP holdings without liquidating the underlying XRP position.

At the time, the account held 751 XRP valued at approximately $1,000, while ETH traded near $2,321.

Instead of selling XRP, the strategy used XRP as collateral for selling ETH put options.

The initial exposure size was approximately equivalent to 1 ETH, meaning the structure carried leverage exceeding 2x relative to collateral value.

This was intentionally aggressive.

But from the beginning, the plan was never simply to “…

Fine-Tuning ETH Options Bot: Adding RSI-Based Assignment Logic

| Algo Trading | 55 seen

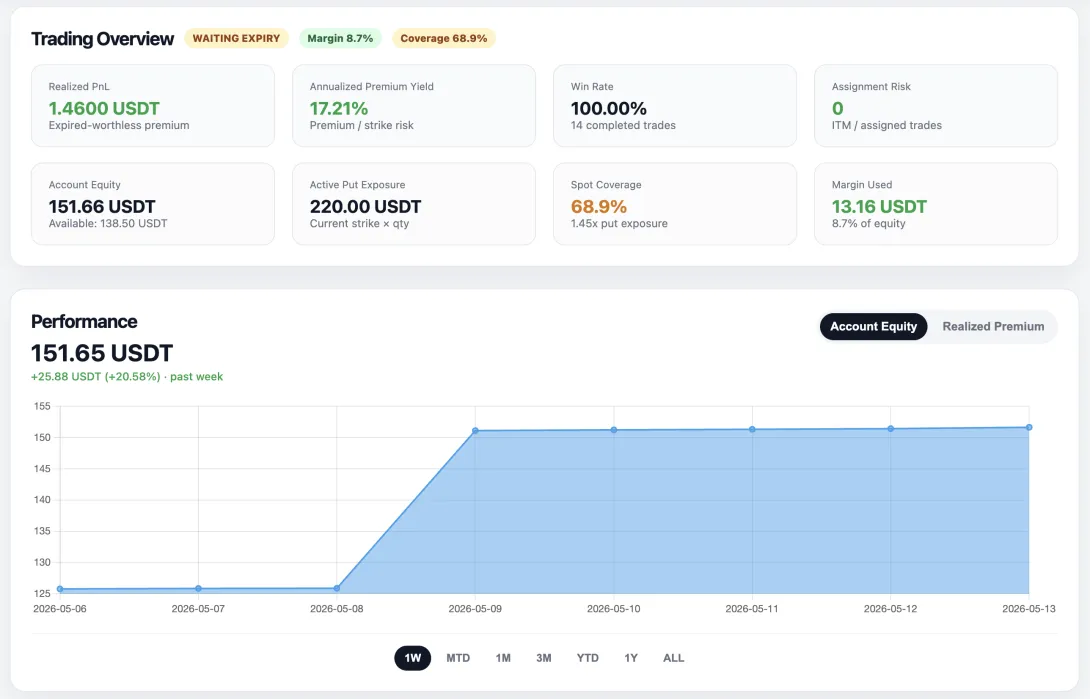

After two weeks of live testing and iteration, we made another meaningful upgrade to our algo trading bot.

For the past 14 days, the Terramatris ETH options engine has been running continuously in production, managing short-duration ETH put strategies on Bybit.

So far, results have been encouraging: the bot has maintained a 100% win rate during the initial live testing period while automatically managing expiries, scanning new opportunities, rolling winning positions forward, and tracking performance metrics in real time.

But despite the strong early performance, one important question remained: What should the bot do when a put option expires in the money?

The Problem With Blind AssignmentInitially, the logic was simple:

If the option expired worthless…1 DTE ETH Options Trading Bot For Bybit

| Algo Trading | 31 seen

We have started building a 1 DTE ETH options trading bot for Bybit, with the flexibility to extend to Deribit and potentially any exchange that offers an options chain and API access.

Bybit is the primary focus, as it’s where most options trading for the Terramatris crypto hedge fund currently takes place.

In the early days of Terramatris, the options strategy was entirely manual. I focused on trading 1 DTE Ethereum options, primarily selling far out-of-the-money contracts with very low delta.

Over roughly a one-year period, the performance was surprisingly consistent. Only about 5–6 trades—with delta below -0.1—were meaningfully challenged.

That said, those weren’t truly systematic trades. They were entered manually, driven by human judgment—and at times,…

Backtesting Ethereum: How Often Does ETH Drop 5% in a Day?

| Research | 43 seen

While working with the TerraM trading bot, I conducted a backtest to quantify the frequency of significant daily drawdowns over the past 365 days (May 4, 2025 – May 3, 2026). Specifically, I analyzed how often the daily price change exceeded -5% or more. The results are notable.

The dataset is based on historical price data sourced from CoinMarketCap, with calculations performed in Google Sheets. Daily performance was measured as the percentage change between the open and close prices.

Out of 365 trading days—reflecting the continuous nature of crypto markets—194 days closed negative, while 171 days were positive. This distribution suggests a moderately bearish environment over the observed period, consistent with broader market conditions.

Distribution of Daily…Crypto Meetup in Palolem Beach, Goa – Traders, Builders & Investors Welcome

| Events | 57 seen

Join us for an informal, high-quality crypto meetup right on Palolem Beach, South Goa. This gathering brings together traders, builders, researchers, and open-minded enthusiasts for a focused discussion on real market strategies and emerging opportunities.

When: Thursday, December 25 12:00 PM - 2:00 PM (GMT+5:30)Where: Palolem Beach, GoaTopics on the table

Crypto options trading (practical strategies, risk frameworks, yield ideas)DeFi staking/yields and what currently worksBitcoin, Ethereum, Solana market outlooksAnalysis of promising altcoins with real potentialOpen discussion: what’s worth watching in 2026?Format

Straightforward conversations, shared insights, and a few Kingfishers in between.

Who’s welcome

Anyone serious about crypto: traders…

Crypto Options Prediction Bot — Inside Our Next-Gen AI Trading Engine

| Algo Trading | 112 seen

At Terramatris, we’ve spent years exploring the intersection of quantitative finance, machine learning, and blockchain markets.

Our latest internal project - Crypto Options Prediction Bot - represents a major leap in how AI can analyze and rank crypto options across Deribit in real time.

Unlike retail “signal” bots, our bot doesn’t guess. it learns, measures, and scores every BTC and ETH options contract based on statistical probabilities, expected returns, and volatility dynamics.

Fetches live Deribit options data for BTC and ETH every week.Filters all contracts with Friday expiries — matching standard options cycles.Uses machine learning models to estimate:The probability an option expires out-of-the-money (P(OTM))Its expected return (%)Liquidity and volatility…