Blog

Crypto Options Selling Ideas for November 7, 2025 – Cash-Secured Puts & Covered Calls

| Crypto Options | 10 seen

Welcome to the first weekly newsletter from Terramatris Research, where we highlight potential trade candidates discovered by our in-house options scanner at scanner.terramatris.eu.

Each week, our screening engine evaluates crypto options across BTC, ETH, and selected altcoins to identify premium-selling setups with favorable risk-to-reward and a statistically high chance of expiring worthless.

In this inaugural edition, we focus on simple option-selling strategies:

Cash-secured puts – for traders comfortable owning the underlying at a discount.

Covered calls – for those already holding the asset and seeking to earn additional yield.

We do not recommend selling naked call options under any circumstances, and we strongly discourage the use of significant leverage. If you choose to apply leverage, keep it minimal — think 1.1 ×, not 5 ×. The objective here is steady, compounding premium income, not gambling on volatility spikes.

Without further ado, here are this week’s trade ideas our scanner flagged as potentially profitable, high-probability candidates for expiration without value.

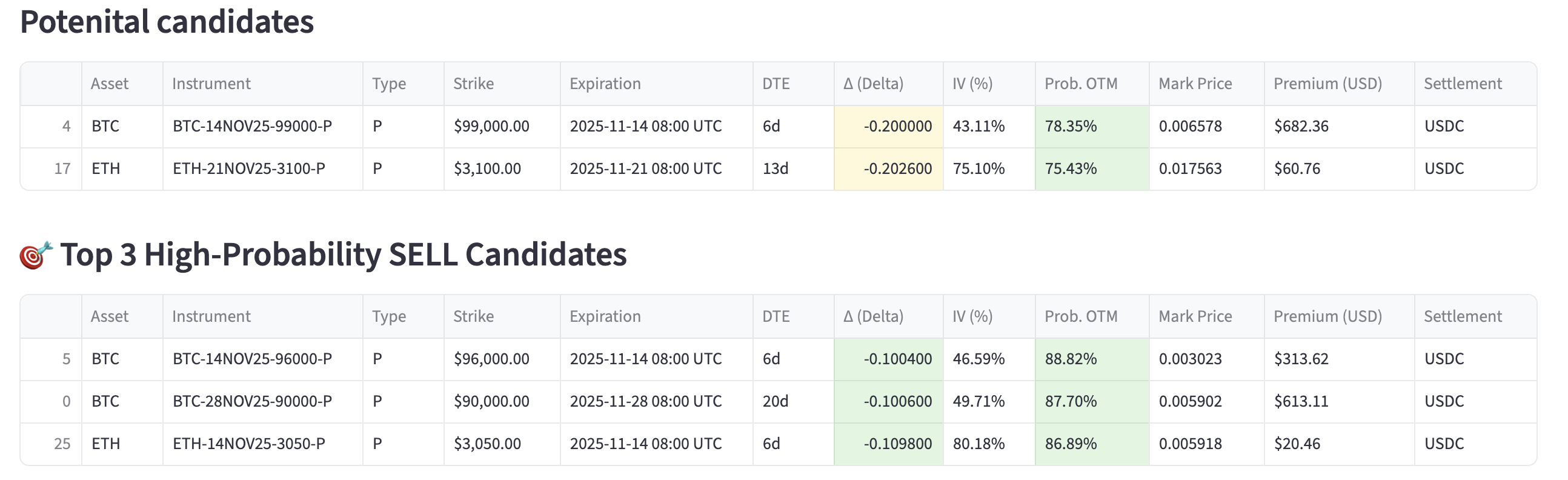

Trade Recommendations – Week of November 7, 2025

This week’s Terramatris Options Scanner identified several high-probability premium-selling setups with attractive implied volatility and strong probabilities of expiring worthless.

We focus only on short-premium strategies — selling puts and covered calls — that align with our conservative, income-oriented approach. All probabilities are derived from real-time Deribit option data; values such as delta, IV, and mark price are included for reference.

Cash secured puts

All listed trades show probabilities of expiring OTM above 75 %, indicating favorable odds for option sellers.

BTC’s short-dated puts offer tighter spreads and lower margin requirements, while ETH continues to price in elevated volatility, rewarding premium collectors who manage risk carefully.

We recommend sticking with cash-secured puts and covered calls, avoiding naked positions. Use small size relative to total capital — think 1–5 % risk per leg, no leverage, and be prepared to take assignment if prices drop.

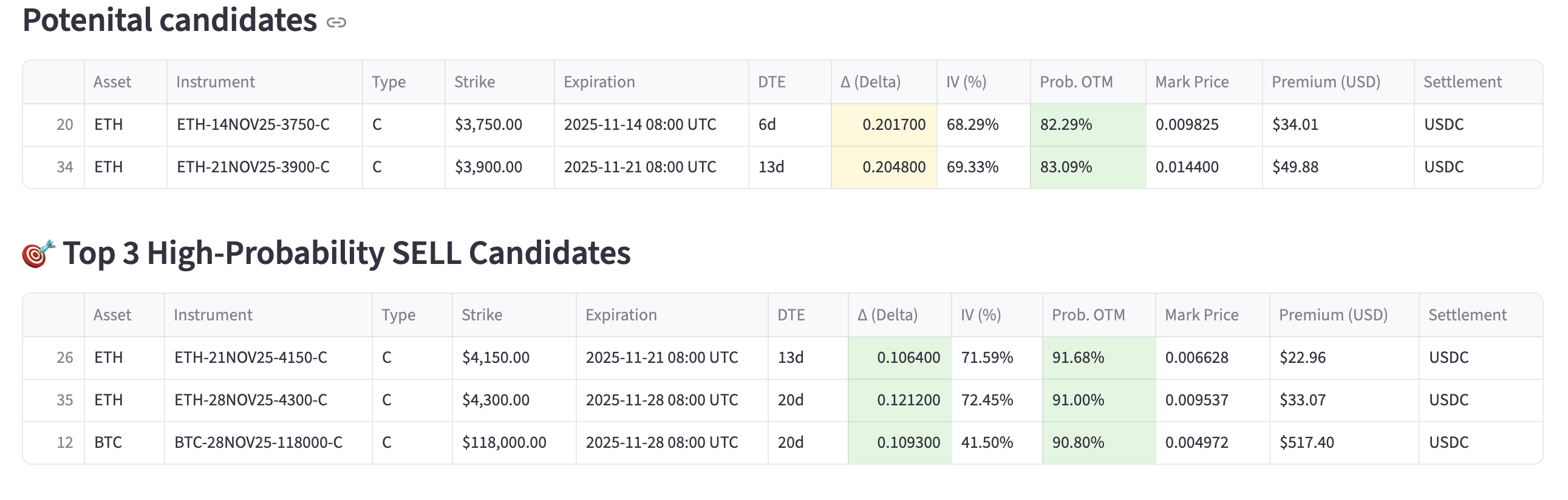

Covered calls

All the listed positions have probabilities of expiring out-of-the-money above 80 %, making them strong candidates for covered-call premium collection rather than naked call sales.

ETH remains the richer volatility target, offering better call-selling yields.

BTC premiums are lower in relative terms but stable and suitable for conservative covered-call exposure.

All trades carry high OTM probabilities (> 90 % on the top picks).

The focus remains on covered calls only — avoid naked call exposure, especially with IV above 70 %.

As always, use small allocation per leg (≈ 5 % of portfolio) and avoid leverage.

Next week, we’ll review the outcomes of these trades and, if needed, adjust the parameters of our options scanner to better align with evolving market volatility.

Never miss an update! Get weekly insights delivered to your inbox—subscribe to the Crypto Options newsletter

How to Repair a Deep-in-the-Money Covered Call in Crypto

| Crypto Options | 37 seen

Covered calls are among the most reliable tools for extracting yield in volatile markets. Still, when prices fall sharply, even disciplined positions face pressure. The decision then shifts from profit maximization to risk control and capital efficiency.

In this article, we’ll walk through practical ways to repair a broken covered call, especially when the underlying asset has crashed and the position is deep in the money.

At Terramatris, we primarily trade crypto options, so the examples focus on assets like Ethereum — but the same principles apply to traditional stock covered calls as well.

1. Rolling Down the Call

When the underlying declines, the short call’s value drops. Buying it back and reselling at a lower strike increases income but sacrifices potential upside if prices recover. It’s a quick income fix, not a long-term solution.

2. Ratio Rolling (Adding Lower Calls)

Selling an additional lower strike call can speed up premium recovery but doubles exposure if the market reverses. It’s a tactic that rewards precision timing and disciplined risk sizing.

3. Closing and Re-Entering via Short Puts

Closing the covered call and pivoting to short puts allows traders to maintain premium flow while resetting exposure lower. It’s often cleaner when volatility remains high and directional conviction is low.

At Terramatris, we operate under a simple principle: Income first, precision later.

We’re comfortable selling aggressive calls below breakeven to maintain premium inflow — but only when risk/reward justifies it. Our breakeven on ETH is roughly $4,250, and we’re currently evaluating selling short-term calls with $3,600–$3,800 strikes while the market stabilizes around $3,200–$3,300.

This approach acknowledges near-term downside risk while extracting yield from elevated implied volatility. If the market recovers and ETH closes above the strike:

- Assignment at $3,600–$3,800 would effectively realize a controlled loss versus our original $4,250 entry.

- From there, we’d re-enter exposure via short puts, likely around $3,000–$3,200, collecting premium while positioning to rebuild ownership at a better cost basis.

This keeps the capital working without forcing early exits or reactive hedges.

When ETH plunged from ~$4,100 to $3,200, our 1 ETH covered call was deep underwater relative to the initial entry. Rather than panic-selling, we analyzed the probability curve:

- At-the-money IV was above 80%, creating strong short premium opportunities.

- Selling 1-week calls around $3,600–$3,700 would yield roughly $38–$56 per contract, translating to a 1–1.5% return on notional for a single week.

That’s sufficient to reduce the effective cost basis toward $4,200 even if price drifts sideways. If assigned, the follow-up short put cycle continues the yield chain without margin strain.

We’ve long maintained that leverage is a double-edged sword. It amplifies gains in quiet markets but can destroy capital during volatility spikes.

As the Terramatris portfolio grows, our objective is clear:

- Keep leverage lower, ideally under 1.2× net exposure.

- Prioritize liquidity and optionality over absolute yield.

- Let compounded option income grow the portfolio organically, rather than force size with borrowed capital.

Reducing leverage allows us to survive drawdowns intact — which, in option writing, is the real competitive edge.

Covered call “repair” isn’t about recovering every lost dollar — it’s about managing premium flow and risk posture intelligently. At Terramatris, we remain patient. We’re evaluating short calls between $3,500–$3,600, not rushing to sell. If assignment occurs, we’ll pivot to short puts near $3,000–$3,200 to re-establish long exposure with lower basis and continued yield.

In volatile markets, survival and steady premium accumulation matter more than speed.

Solana Covered Call Growth Fund Performance - October 2025

| Funds | 23 seen

The Terramatris Solana Covered Calls Growth Fund completed its second full month of operations in October 2025. The Fund continued to follow its systematic covered call strategy on Solana (SOL), maintaining disciplined position management amid heightened crypto market volatility.

By the end of October, the Fund had 12,171 shares issued, bringing total Assets Under Management (AUM) to $10,831 based on a closing NAV of $0.89 per share. This represents a 95.6% increase in AUM from September’s level of $5,536.

Solana’s market price declined from $208 to $186 (-10.6%) over the month, while the Fund’s NAV decreased 4.3%, demonstrating relative resilience and approximately +6.3% outperformance versus the underlying asset.

The Fund remains open to new capital commitments until total AUM reaches $100,000. TerraM Fund, one of our core investors, continues biweekly contributions of $100, supporting consistent capital growth.

For full details on Fund activity, performance, and strategy outlook, please refer to the attached monthly report.

Poor Man’s Crypto Hedge Fund: Earning Income from Dogecoin Options on Bybit

| Crypto Options | 17 seen

After Bybit enabled options trading for Dogecoin (DOGE), we decided to include DOGE in the TerraM Multi-Asset Crypto Options Fund. Our favorite approach across assets remains consistent - selling put options to generate income and using that income to accumulate the underlying asset over time.

If assigned, we take delivery of the asset and sell covered calls. More often than not, we roll forward the position for a credit instead of letting the call get exercised, effectively compounding income while maintaining exposure.

On October 29, we opened our first DOGE position by selling:

- 1,000 DOGE put options

- Strike: $0.185

- Credit received: $0.019 per DOGE

- Expiry: October 31, 2025

By October 31, the strike was in the money, so we decided to take a proactive stance — rolling the position forward one week to the next expiry while lowering the strike price to $0.18 and earning an additional premium of $0.0058 per DOGE.

All collected premium is reinvested into spot DOGE, which is now part of our TerraM Multi-Asset fund.

- Spot DOGE holdings: 40 DOGE

- Short puts: 1,000 contracts (strike $0.18)

- Average buy price: $0.1895

- Break-even price: $0.1742

What happens next?

If, on expiry — November 7, 2025, DOGE remains above $0.18, our short put options will expire worthless, allowing us to keep the full premium and continue selling new weekly puts to generate consistent income.

If, however, DOGE trades below $0.18, we’ll evaluate two possible paths:

- Roll Out and Forward: Extend the position to a later expiry while keeping or slightly adjusting the strike price — ideally for an additional net credit, compounding the income stream.

- Take Assignment: Accept delivery, most likely in the form of a perpetual futures position, and transition to a covered call selling strategy to generate further yield.

This flexible approach allows us to adapt dynamically to market conditions while maintaining our primary goal — steady option income and strategic accumulation of DOGE within the TerraM Multi-Asset Crypto Options Fund.

After our first week with DOGE coin option we are looking at 3% income in 9 days

This marks the start of our “Poor Man’s Crypto Hedge Fund” series, where we’ll use DOGE as a fun and educational vehicle to demonstrate disciplined, option-based accumulation and yield generation in crypto markets.

As always, all DOGE income and positions are part of the TerraM Multi-Asset Crypto Options Fund, following the same risk-managed, income-compounding approach used with BTC, ETH, and SOL.

Why We Added MNT to Our Long-Term Investment Portfolio

| Investment ideas | 15 seen

At Terramatris, we’ve added a small position in Mantle (MNT) to our Multi-Asset Crypto Options Fund, following Bybit’s launch of MNT options. The move aligns perfectly with our focus on assets that support options trading — a key part of our long-term yield strategy.

We’re generally bullish on assets that we can build structured positions around — primarily BTC, ETH, and SOL — since these allow us to generate steady yield through systematic option selling. Seeing MNT appear on Bybit’s options chain was a bit unexpected, but it instantly put the project on our radar.

Mantle brings together a modular Ethereum Layer-2 design, a growing DeFi ecosystem, and now — importantly for us — derivative market access. That last point makes all the difference for an options-based strategy like ours.

We began by establishing a small position via put options, collecting premiums and using part of the earned premium to accumulate spot MNT for our long-term holdings. This approach lets us scale exposure gradually, with downside protection and steady income generation — consistent with how we’ve built other long-term crypto positions in the fund.

We’re not in the business of making short-term price predictions, but we did run a few internal simulations on potential valuation ranges. Seeing MNT in the $10–$20 price range appears much more realistic than $100. Still, we do enjoy a good moonshot, and if Mantle reaches triple digits someday, we’ll gladly ride that wave.

Alongside our options exposure, we’re also exploring DeFi opportunities for MNT staking within the Mantle ecosystem and beyond. Generating additional passive yield through on-chain protocols complements our options-based income, helping us compound returns while supporting ecosystem growth.

Our MNT position is modest but strategic. The introduction of options trading gives Mantle a new level of market maturity, and for Terramatris, that’s a clear signal to start paying attention. As always, we’ll continue to sell options, collect yield, and build spot exposure over time — one premium at a time.

Introducing Terramatris SMA — Expanding Opportunities in Tailored Crypto Management

| Crypto Options | 17 seen

At Terramatris, our journey has always been rooted in one clear goal — to grow capital through options trading. From day one, our focus has been on developing strategies that generate consistent, risk-adjusted returns in the ever-evolving crypto derivatives market.

In our early days, we briefly explored managing client portfolios through Separately Managed Accounts (SMAs). While that initiative never really took off at the time, it gave us valuable insights into the infrastructure, compliance, and communication needed to manage external capital effectively. Over the years, we instead found stronger growth in pooled asset management, developing scalable structures and robust strategies through our core vehicles — the TerraM Multi-Asset Crypto Options Fund, the Solana Covered Call Growth Fund, and our native TerraM token.

Now, with a mature foundation, proven execution systems, and increased client interest, we are pleased to offer Terramatris SMA — a fully personalized solution for investors who prefer direct account management while benefiting from our expertise in options-based yield generation.

SMA Offering Highlights

- Minimum Investment: $25,000

- Strategy Focus: Options-selling and volatility strategies on BTC, ETH, SOL, XRP, DOGE, and MNT

- Execution Platforms: We operate across leading derivatives and spot exchanges including Deribit, Bybit, Deriv, Gate.io, and Binance

- Flexible Structure: Accounts can be connected via API integration or managed through direct execution, depending on client preference

- Transparency and Control: Investors retain full ownership and real-time visibility over their capital, while Terramatris provides ongoing strategy management and reporting

Built in Partnership with Our Clients

Each SMA is managed in close collaboration with the client. From initial strategy design to live portfolio monitoring, we emphasize transparency, flexibility, and clear communication. This ensures that every trading decision reflects both market conditions and the investor’s specific objectives.

A Natural Step Forward

While our primary focus remains on growing the Terramatris ecosystem through our funds and native token, the SMA offering is a strategic expansion — a way to extend our proven trading framework to a select group of investors seeking tailored solutions.

At Terramatris, we see SMAs as a continuation of our mission: leveraging advanced options trading to grow capital efficiently, responsibly, and transparently — now with an individualized touch.

Bybit to Launch XRP Options — A New Opportunity Ahead

| Crypto Options | 36 seen

During our routine login to Bybit today, we noticed an exciting update: Bybit will be adding XRP options contracts starting October 21.

At this stage, there’s limited public information about contract specifications, such as lot size, expiry intervals, or margin terms. However, the announcement itself is noteworthy, especially considering XRP’s growing liquidity and Bybit’s increasing dominance in the crypto derivatives space.

Although the Terramatris Fund currently does not hold XRP directly, this development could influence our positioning in the near future. Bybit has long been one of our go-to platforms for options trading, and depending on the contract size and leverage terms, we may explore credit spreads or covered call strategies on XRP once the instruments become available.

Overall, this is a welcome addition to the crypto options landscape — and we’ll be watching closely how the market responds once trading opens on October 21.

How Crypto Reacts to U.S. Tariff Announcements — and Why It Hurts More Than Stocks

| Research | 46 seen

When the U.S. government announces new tariffs, markets panic, and crypto tends to take the hardest hit.

We’ve seen this pattern repeatedly: a single policy shock sends stocks tumbling, bonds rallying, and Bitcoin plunging twice as hard. But why does a trade policy aimed at physical goods ripple so violently through digital assets? And how long does it usually take for crypto to recover?

Let’s break down the dynamics, the psychology, and what we’ve observed firsthand in our own portfolio after major tariff shocks.

The Immediate Reaction: Panic, Liquidations, and Correlation

Tariff announcements are not just about economics — they’re about uncertainty.

The moment new import taxes or trade restrictions are declared, global investors shift into “risk-off” mode. Equities fall, the dollar spikes, and liquidity evaporates across speculative assets.

Crypto, unfortunately, sits at the very edge of that spectrum.

Within hours of such announcements:

- Bitcoin and Ethereum typically drop 2–3× more than the S&P 500.

- Open interest on futures markets collapses.

- Billions in leveraged long positions are liquidated.

- Volatility (realized and implied) explodes.

In our experience at Terramatris, the portfolio often suffers its sharpest daily drawdowns during tariff headlines — even though the crypto market has no direct link to steel, cars, or semiconductors.

This is purely a sentiment correlation effect: when traditional traders de-risk, they sell everything with volatility attached — and crypto is at the top of that list.

Why Crypto Reacts to Trade Policy at All

There are three main mechanisms behind this correlation:

Risk sentiment transfer

Crypto now trades as a global risk asset. Institutional money, macro funds, and retail traders all treat Bitcoin and Ethereum as high-beta plays on liquidity and optimism. When tariff news signals slower growth or global uncertainty, those positions are first to go.

Liquidity chain effect

Margin calls and equity losses force fund managers to raise cash elsewhere. Crypto holdings — especially on regulated platforms — are often liquidated to meet collateral needs.

Narrative contagion

Even if tariffs don’t touch crypto directly, the macro narrative shifts from “expansion” to “recession risk.” That shift compresses valuations across all risk assets. Algorithms trading cross-asset correlations simply follow the flow.

How Long It Usually Takes to Recover

Looking at previous episodes (2018 China tariffs, 2019 escalation, and smaller tariff scares since), crypto tends to follow a three-phase recovery pattern:

Shock & liquidation

1–3 days

Sharp 10–20 % drops, high funding rates reset, huge volumes

Relief rebound

3–10 days

Oversold bounce, short-covering, funding normalizes

Consolidation & rebuild

2–4 weeks

Range trading before resuming trend, often faster than equities

On average, major tariff-induced crypto crashes take about 2–4 weeks to fully recover, assuming no new escalation.

If tariffs deepen or retaliation follows, recovery can stretch to 6–8 weeks.

Interestingly, crypto often leads the recovery phase — once fear subsides, liquidity returns faster to Bitcoin than to equities. But timing it requires patience and strict risk control.

Our Experience: The March–April Drawdown and September Rebound

At Terramatris, we experienced a massive portfolio drop during the March–April 2025 correction, triggered by tariff fears and broader macro stress.

The portfolio lost a significant portion of value within days as leveraged long positions across exchanges were liquidated.

However, by staying disciplined — cutting leverage, keeping exposure manageable, and gradually rebuilding — the market fully recovered and went on to reach new all-time highs by September 2025.

That rebound reinforced a critical lesson:

Leverage is the biggest enemy during macro shocks.

Crypto’s volatility is already extreme; adding borrowed exposure magnifies losses exponentially.

Avoiding leverage — or using it sparingly and strategically — is the single best defense against panic-driven wipeouts.

Why Recovery Sometimes Doesn’t Come Quickly

There are reasons recovery may stall or fail entirely:

- Persistent macro fear: If tariffs escalate into a prolonged trade war, investor appetite for high-volatility assets stays low.

- Tight monetary policy: When interest rates remain high, liquidity to fuel speculative rallies dries up.

- Sentiment damage: Multiple shocks in a short period (tariffs + regulation + earnings misses) can exhaust dip buyers.

- Structural leverage wipeouts: After extreme liquidation events, traders need time to rebuild collateral and confidence.

In those cases, the crypto market may move sideways for months even if prices don’t collapse further.

Our Broader Takeaways

Through multiple tariff cycles, we’ve learned three rules that consistently protect capital:

- Keep leverage near zero when macro risk rises.

- Use volatility spikes to sell options or reposition, not to chase price.

- Expect crypto to bottom before equities — but only after forced liquidations clear.

These principles helped us navigate the March–April drawdown and come out stronger in September.

The Takeaway

Tariff announcements are a reminder that crypto is no longer an isolated niche — it’s part of the global macro risk web.

When traditional markets fear slower trade and tighter liquidity, Bitcoin bleeds with the rest of them.

But unlike industrial stocks, crypto tends to snap back faster, provided the policy shock fades instead of festers.

In other words:

“Tariffs don’t target crypto — but crypto still takes the bullet.”

For disciplined investors, that’s both a warning and an opportunity.

When the panic hits, manage risk. When the dust settles, be ready , because crypto rarely stays down for long.

ASR Reward from JUP Makes Us Happy

| Investment ideas | 28 seen

Sometimes the crypto world brings pleasant surprises — and this week, JUP Network did exactly that for us at Terramatris.

Back in January 2024, JUP tokens unexpectedly landed in our portfolio as part of a surprise airdrop. At the time, we didn’t have any specific stance on the project — we weren’t particularly bullish or bearish.

Jupiter (JUP): Why This Solana DeFi Token Caught Our Attention

We decided to allocate a small portion of our fund to JUP, categorizing it in our “moonshot sector” - assets that we’d be thrilled to see appreciate 10x–100x in a meaningful time frame but are also ready to accept could go to zero. JUP fit perfectly into that high-risk, high-upside segment of our portfolio.

Instead of letting the tokens sit idle, we continued dollar-cost averaging into JUP over time. The tokens we accumulated are staked, and we also participate in the Jupiter DAO, engaging with governance and network updates.

These are not core trading activities for our fund — rather, they represent our contemplative, experimental side, exploring promising ecosystems without risking too much capital.

One of JUP’s most interesting mechanics is its ASR (Active Staking Rewards) system, which distributes rewards once per quarter. We’ve just received our latest round — an estimated 2% in additional tokens and while that might not sound huge, it’s a solid and consistent return for an otherwise passive position.

In a market where many assets promise much but deliver little, these ASR rewards are a reminder that steady participation pays off — even if the total exposure is small.

We don’t see JUP as a pillar of the Terramatris portfolio, but rather as a speculative satellite, orbiting around our more strategic investments. Still, when surprises like this ASR reward arrive, they make us smile and keep us curious about what’s next for the Jupiter ecosystem.

Georgian Tax Residency: A Strategic Option for HNWIs and Crypto Individuals

| Research | 69 seen

At Terramatris, we examine how funds and financial structures work across different jurisdictions. We don’t provide legal or tax advice, but we do explore how certain models stand out in the global landscape. One of the most compelling examples today is Georgia’s tax residency framework, which offers particular advantages to high-net-worth individuals (HNWIs) and crypto investors.

What Is Georgian Tax Residency?

The most common path is the 183-day rule:

- If you spend at least 183 days in Georgia during a rolling 12-month period, you qualify as a tax resident.

There is also a High Net Worth Individual (HNWI) track, where residency can be granted even without the 183 days, provided you can demonstrate certain global income or asset thresholds. This makes Georgia appealing to internationally mobile individuals who do not want to tie themselves down geographically.

The Georgian Revenue Service issues a tax residency certificate, which is critical for establishing Georgia as your tax home in the eyes of other jurisdictions.

Why It Matters for Individuals

Territorial Taxation

Georgia taxes only Georgian-sourced income. For HNWIs and crypto holders whose wealth is generated abroad (for example, from trading on international exchanges), this can dramatically reduce tax burdens.

Crypto-Friendly Environment

Georgia has signaled openness toward digital assets. While regulations are evolving, the environment remains relatively light compared to more restrictive countries.

Flat and Simple Personal Taxes

Georgian-sourced income is taxed at a flat 20%, while certain statuses (such as small business regime) can lower effective taxation significantly. For individuals with mixed income streams, the simplicity is attractive.

Wealth Protection & Lifestyle

Residency in Georgia offers more than taxes: low cost of living, access to banking, and a strategic location between Europe and Asia. For individuals seeking to diversify lifestyle and financial risk, this creates added resilience.

Potential Downsides to Consider

No jurisdiction is perfect. Before considering Georgian tax residency, individuals should be aware of the following limitations:

Changing Regulations

Georgia is still shaping its crypto policy and broader financial regulations. What looks advantageous today may be revised in the future as global standards tighten.

Perception of Tax Residency

Other countries may not automatically recognize Georgia as your main tax base if you maintain strong ties elsewhere (property, family, business). This can lead to dual-taxation disputes, especially with more aggressive tax authorities.

Banking & Financial Services

Although Georgia’s banking system is accessible, it is not as internationally integrated as Switzerland, Luxembourg, or Singapore. Large crypto-to-fiat transactions may attract scrutiny.

HNWI Track Limitations

Proving wealth or income for the HNWI residency track requires documentation and sometimes discretionary approval. It may not be as straightforward as the 183-day rule.

Reputation Risks

Some investors may view Georgia as an “emerging” jurisdiction rather than a fully established financial hub. This perception can matter when dealing with conservative institutions or international partners.

Relevance for Crypto Individuals

Unlike funds or firms — which we’ve discussed separately in our article on crypto fund structures and Georgia’s role — individual investors face different challenges. Residency and taxation directly impact how profits from trading, long-term holding, and portfolio rebalancing are treated.

For a crypto individual:

- Establishing Georgia as your primary tax residence can help avoid dual-taxation conflicts.

- Gains from foreign crypto trades may fall outside Georgian taxation under the territorial system.

- The HNWI track provides flexibility for those who prefer not to spend long periods in one country.

Important Caveat

As always, Terramatris emphasizes: we are not providing legal or tax advice. Each person must consult qualified advisors before acting. Our goal is to analyze global financial structures, and Georgia stands out as a particularly innovative jurisdiction for individuals navigating the complexities of crypto wealth.

For HNWIs and crypto individuals, Georgia offers a unique mix: territorial taxation, flexibility in residency options, and a crypto-friendly outlook. But with potential downsides — from regulatory changes to perception risks — careful planning is essential.

At Terramatris, we see the Georgian tax model as one of the most interesting cases globally, and one that deserves close attention from anyone serious about cross-border wealth and crypto management.

And for anyone going through the process, a great helper for tax document translations and notarization services is caucasustranslations.com.

Why Registering a Small Crypto Trading Firm in Georgia Makes Sense

| Research | 26 seen

The global crypto market is becoming more institutionalized, and even small proprietary trading firms need to think about jurisdiction, compliance, and taxation. While the U.S. (Wyoming, Delaware) and offshore hubs (BVI, Seychelles) remain popular, Georgia, the country in the Caucasus,has quietly emerged as an attractive option for crypto-friendly businesses.

Below, we’ll explore why Georgia might make sense for a small crypto trading firm, what the registration process looks like, and the pros and considerations you should keep in mind.

Why Georgia?

Crypto-friendly environment: Georgia does not have hostile legislation toward crypto. Trading, investing, and holding digital assets is not restricted for companies or individuals.

Low taxes: Georgia applies an Estonian-style corporate tax model — you only pay corporate tax (15%) when distributing profits as dividends. Reinvested earnings are tax-free. For small businesses, a turnover tax regime exists with just 1% tax on revenue if annual turnover is under GEL 500,000 (~USD 180,000).

Banking access: Unlike some offshore jurisdictions, Georgian banks (TBC, Bank of Georgia) are relatively open to fintech and international clients.

Ease of incorporation: An LLC can be registered in a few days. Remote registration is possible through a power of attorney.

Steps to Register a Trading Firm in Georgia

Incorporation

- File Articles of Association and register with the National Agency of Public Registry.

- Typical turnaround: 1–2 business days.

Tax ID & VAT Status

- Obtain a tax identification number.

- For small trading firms, VAT may not be required, but it depends on your turnover and activities.

Bank Account

- Open a corporate account at a Georgian bank (TBC, Bank of Georgia).

- Alternatively, apply to fintech solutions like Wise or Payoneer for global transfers.

Exchange Accounts (Corporate KYB)

- Exchanges like Bybit and Deribit allow corporate accounts.

- Provide incorporation docs, tax ID, and proof of ownership.

Compliance & Reporting

- Maintain accounting records.

- File annual reports; tax only applies when distributing profits.

Tax Advantages

Reinvestment Freedom: Retained earnings are tax-free until distributed. Perfect for proprietary firms reinvesting in crypto.

Small Business Regime: Under GEL 500,000 turnover, pay 1% turnover tax instead of standard rates.

Dividend Withholding Tax: When distributing profits, an additional 5% applies, making the effective tax burden about 20% — still competitive globally.

Considerations and Challenges

Enhanced banking oversight: Financial institutions in Georgia, like in many jurisdictions, apply rigorous due diligence for companies engaged in digital assets. Firms should be prepared to provide clear documentation and transparency in operations.

Evolving regulatory framework: While crypto activity is currently accommodated within existing structures, digital asset regulation worldwide continues to develop. Firms should anticipate potential adjustments and align with international compliance standards.

Operational requirements: Maintaining proper accounting, local reporting, and engaging qualified advisors is essential for full compliance and efficient tax planning.

For a small proprietary crypto trading firm, Georgia offers a combination of low taxation, ease of registration, and access to international banking that few jurisdictions can match. It is particularly compelling for firms reinvesting profits into spot crypto rather than distributing dividends frequently.

Important Note: We are not offering legal, tax, or incorporation services in Georgia. This article is for informational purposes only. However, if you are considering setting up a small trading firm and would like to have a meaningful conversation about structuring, strategy, and practical experiences, we would be open to a discussion.

Discovering Derive: Our First Steps into True DEX Options Trading

| Research | 24 seen

At Terramatris, we’ve always been fascinated by the evolution of crypto markets and the growing range of opportunities they create for traders and investors. For years, our main focus has been on more traditional centralized exchanges (CEX) such as Bybit and Deribit. These platforms have provided liquidity, stability, and advanced trading features—making them indispensable for our operations.

But one thing has always been missing: a true decentralized exchange (DEX) for options trading.

Recently, while researching potential institutional partners for our US operations (Kraken), we stumbled upon Derive, a DEX options trading platform. If liquidity and market makers keep growing, Derive has the potential to become a central piece in the future of decentralized derivatives trading.

Why Derive Matters

Decentralized trading isn’t just about ideology—it’s about resilience, accessibility, and innovation. While we still rely heavily on CEXs for their speed and liquidity, a truly functioning DEX fills a crucial gap. Derive does just that.

At the moment, Derive supports BTC and ETH options trading. Naturally, we would love to see Solana integrated in the future, especially since we’re actively running our Solana Covered Call Growth Fund. But even without Solana, having BTC and ETH live on a fully decentralized platform is an exciting step forward.

The fee structure is another point of interest. On first glance, trading fees seem higher compared to centralized competitors like Bybit or Deribit. However, Derive’s native token (DRV) plays an important role. Traders receive partial refunds in DRV, effectively cutting fees in half. For us, this means not only do we get exposure to a new instrument (DEX options), but we also add a new token to our portfolio. We see this as a learning opportunity, and we’re happy to take a small position as we continue exploring the ecosystem.

Who’s Behind Derive?

As we dug deeper, we learned that Derive is backed by the Lyra Foundation, a team known for pioneering decentralized derivatives. While our knowledge so far only scratches the surface, we feel increasingly confident about their vision and execution. It’s rare to find a DEX team that has both the technical expertise and the financial infrastructure to compete with established CEXs.

Our philosophy at Terramatris has always been simple: we like to put our money where our mouth is. That’s why, even at this early stage, we’re committing a small portion of our portfolio to Derive.

How It Works in Practice

Getting started on Derive was straightforward but requires some familiarity with DeFi tools. Here’s how we approached it:

- Wallet Setup – Derive connects through MetaMask, making onboarding seamless for anyone already using DeFi applications.

- Network Choice – We opted for the Arbitrum network, which offered us lower fees and reliable transaction speeds.

- Funding the Account – We deposited USDC and ETH into our wallet on Arbitrum, ensuring we had both stable collateral and trading capital.

- First Trade – To test the waters, we opened a 0.1 ETH put contract. This small initial trade is our way of learning the platform mechanics while limiting risk exposure.

So far, the process has been smooth, and the interface feels intuitive compared to other DEX platforms we’ve tested in the past.

Our First Impressions

- Accessibility: The MetaMask integration is seamless, making it easy for anyone with a Web3 wallet to get started.

- Transparency: No KYC requirements keep the platform true to the spirit of DeFi. But that might be challenging in the future.

- Innovation: The DRV token and fee refund system provide an interesting incentive model, even if it’s something we’re still learning about.

- Potential: If Derive manages to attract enough liquidity, it could become a serious competitor to the established CEXs.

For us, Derive represents more than just another trading platform—it’s a proof of concept that decentralized options trading can work. While we still rely on centralized exchanges for the majority of our trading activity, having a DEX option is something we’ve been waiting for.

We are genuinely excited about this development. Even though our current position is small, it feels like the beginning of something important. In the future, we would love to see Solana integrated, which would align perfectly with our existing strategies.

For now, Derive has already earned a spot in our portfolio and in our watchlist. It’s rare that we come across something that feels both innovative and practical—but Derive checks both boxes.

As always, we’ll continue to share our journey and learnings with our community. If you’re curious about decentralized options trading, we encourage you to give Derive a try—all you need is MetaMask and some ETH.

Why We Added Wormhole (W) to the TerraM Portfolio?

| Investment ideas | 44 seen

At Terramatris, our core strategy is straightforward: we focus on established assets like Bitcoin, Ethereum, and Solana, and we use them to generate a steady flow of options premium. That premium is what drives our consistency. It’s boring, it works, and it’s repeatable.

But there’s another side to our strategy. We also keep a sleeve of moonshot bets — small, speculative positions that could one day turn into something much larger. The logic is simple: in crypto, a single asymmetric bet can change the shape of the portfolio. We’re not reckless, but we are opportunistic.

How Wormhole Landed on Our Radar

We like to make the discovery process fun. Instead of pretending we can out-research every token ourselves, we let AI help us dig. (Thank you, ChatGPT.)

The process brought us to Wormhole (W), an interoperability protocol connecting more than 20 blockchains. Does it become the TCP/IP of crypto? Or does it get outcompeted? Honestly — we don’t know. That’s exactly why it fits in the moonshot sleeve.

Our belief in Wormhole is neutral. We don’t say “yes” or “no.” We just recognize the possibility that today’s small bet could become tomorrow’s big win — or fade into nothing. That’s the asymmetric tradeoff we’re looking for.

From Pengu to Wormhole

Earlier this year, we allocated to another speculative token — Pengu. After raising 5,000 Pengu in our portfolio, we decided it was time to rotate into a fresh opportunity. The replacement? Wormhole.

At current prices, we’re targeting an allocation of 2,000–3,000 W tokens in 2025 before reassessing. The sizing is intentionally small: enough to matter if it works, but never large enough to endanger the core fund.

Funding Arbitrage

We didn’t just buy spot W. To make things more interesting, we started with a funding fee trade:

- Buy spot W

- Sell perpetual W contracts

This simple arbitrage setup allows us to collect funding fees in the form of W itself. Today, those fees are tiny. But over time? Who knows. Maybe they turn into a meaningful kicker, maybe not. Either way, it’s a low-risk way to enhance the position while staying neutral on short-term price moves.

The Opportunistic Outlook

Our core remains BTC, ETH, and Solana — the proven majors that power the fund. They’re the workhorses generating the premium we rely on.

But we’ll continue to take small, opportunistic bets. Some will fail. Some may deliver 10x, 50x, or more. That’s the nature of moonshots.

Wormhole is simply the latest entry into this sleeve. It could be glue for a multi-chain crypto future, or just another protocol that fades. Either way, we’re in with eyes wide open, position size under control, and curiosity intact.

In short: Wormhole is not our conviction core holding. It’s a deliberate experiment — a small seed planted in 2025, left to see if it grows.

Why We Decided Not Yet to Tokenize Our Solana Covered Call Fund

| Research | 34 seen

When we launched the Solana Covered Call Growth fund, one of the exciting questions on the table was tokenization. The idea of creating a fully on-chain, tokenized representation of fund shares is appealing: transparency, liquidity, and a modern Web3-native structure. However, after careful consideration, we decided not to tokenize—at least not yet.

We are still in the early stages of building and refining this strategy. At this stage, our focus is on performance, repeatability, and reporting, rather than infrastructure. Tokenization can add a layer of complexity—both technical and regulatory—that distracts from the main goal: executing our options strategy consistently and profitably.

We did explore how tokenization could work in practice. For example, we spent several hours testing with Squads, one of the best DAO and treasury tools on Solana. The experience confirmed that while the tech is powerful, it also requires commitment to developer resources, maintenance, and onboarding—all of which might be premature for us.

Instead of rushing into tokenization, we decided to stick with a more traditional approach for now:

- Personal, direct NAV reporting to our investors.

- Simple and clear communication about fund performance.

- Avoiding overhead and not burning resources on developer teams.

This also aligns with our lean early-stage philosophy: we want to deploy capital efficiently, not on infrastructure we may not yet need.

What excites us is that we can already operate efficiently and transparently without heavy dev costs. Tools like ChatGPT help us with reporting, automation, and investor communication. This allows us to move fast, keep costs low, and focus on strategy execution.

Our decision is not a rejection of tokenization. We see clear benefits in the long run, and tokenization will likely play a role in the future of this fund. But timing matters. For now, we’re confident that a personal, streamlined, and cost-effective approach best serves our investors.

In short: we chose to walk before we run. Tokenization remains on the horizon, but today our energy is better spent on building trust, delivering returns, and refining our core process.

Delta-Neutral Arbitrage in Crypto: Inside Terramatris Solana Strategy

| Research | 32 seen

At Terramatris, we are still an early-stage crypto hedge fund. Our core strategy leans toward directional exposure—going long on assets we believe in and applying quantitative options strategies to generate income. Specifically, we sell puts and calls on assets like Ethereum and Solana, capturing option premiums while managing risk.

This allows us to grow the fund more aggressively, as we participate directly in upside movements while securing steady cash flow from option sales.

However, as outside capital gradually flows into the fund, we are also introducing arbitrage strategies alongside our directional and options trades. These arbitrage trades are not designed to rapidly grow a small fund, but they add balance, protection, and consistency to our overall portfolio.

Why Arbitrage Matters

Arbitrage trades offer a delta-neutral position, meaning the overall market direction doesn’t affect the outcome. Instead, returns are locked in by capturing spreads between different markets or instruments. While these trades may seem modest in terms of short-term profit, they provide peace of mind and stability for investors who value risk-adjusted returns over volatility.

From a more classical investment perspective, arbitrage can be very lucrative. Some of our strategies—like those in Solana markets—can reach annualized yields of around 9%, which is a strong, consistent return profile compared to many traditional asset classes.

Our Preferred Arbitrage Trade: Solana Spot vs. Futures

One specific trade we enjoy is:

- Long spot SOL (holding Solana directly)

- Shorting Solana futures with a set expiry

This structure allows us to lock in the spread between spot and futures prices, effectively hedging away price movements while securing a predictable yield.

Such trades don’t move the needle much when working with small amounts of capital, but with larger inflows they become a reliable way to enhance the fund’s stability and protect against sharp market swings.

Where We Use These Trades

Currently, arbitrage plays an important role in our Solana Covered Call Growth Fund, where they complement both our long positions and our quantitative options strategies. Looking ahead, we may consider launching a dedicated arbitrage fund. However, that approach would be more capital-intensive—since arbitrage yields scale best with size—and at this stage, our focus is still on growing assets under management.

Conclusion

At Terramatris, we believe in combining growth-oriented directional trades, quantitative options strategies, and risk-managed arbitrage trades. This blended approach allows us to capture market upside while offering investors stability and reliable returns. As our fund grows, we expect arbitrage to play an even more prominent role, potentially shaping entire fund structures dedicated to such strategies.

Why We Decided to Invest in Liberland Dollar (LLD)

| Investment ideas | 54 seen

At Terramatris, we are always exploring opportunities that align with our values of innovation, independence, and forward-thinking. Sometimes, these discoveries come through structured research, and sometimes they appear unexpectedly. Our recent investment into Liberland Dollar (LLD) belongs to the second category — a pleasant surprise during our ongoing research into projects that combine crypto innovation with strong community values.

Over the past year, we’ve attended few crypto-related meetups and brunches in Tbilisi, Georgia, a city that has become a lively hub for blockchain conversations. At nearly every event, we’ve run into Samuela, an enthusiastic Czech representative of Liberland, who passionately shares updates about the micronation and its ambitions.

At one of our recent gatherings, Sam shared some updates about Liberland. While going through them, we discovered that Liberland has its own native token — the Liberland Dollar (LLD). That revelation was the spark that pushed us to take a closer look.

What is Liberland?

Liberland, officially known as the Free Republic of Liberland, is a self-proclaimed micronation founded in 2015 by Czech politician Vít Jedlička. It is located in a small piece of no man’s land between Croatia and Serbia, on the west bank of the Danube River.

This territory, historically unclaimed due to border disputes, became a unique opportunity for Liberland to establish itself as a symbol of freedom, minimal governance, and voluntary cooperation. While not officially recognized as a sovereign state by the UN, Liberland has built an active community of supporters worldwide, with ambassadors, representatives, and even its own crypto-driven economy.

The Liberland Dollar (LLD) is part of that vision. It reflects not only an attempt to build an alternative economic system but also a way for supporters to engage with Liberland’s ideals directly through decentralized finance.

At Terramatris, we don’t shy away from unconventional projects. We believe that innovation often comes from unexpected corners. What sold us on LLD was a combination of factors:

- Shared values: Liberland promotes freedom, independence, and voluntary participation — ideas that resonate with the principles of decentralized finance.

- Unexpected discovery: Learning about LLD firsthand from Sam was a reminder that the crypto world is full of hidden gems waiting to be explored.

- DEX availability: Finding out that LLD is already available on Raydium AMM, a Solana-based decentralized exchange, made us even more excited. A true DEX-first token aligns perfectly with our preference for decentralized investments.

This is not a capital-intensive investment for us. Instead, we see it as a supportive, fun, and value-sharing step. At this stage, our goal is to accumulate no less than 100 LLD tokens — a symbolic position that signals our support for Liberland’s vision while keeping exposure modest.

We believe in staying open to diverse projects, and while LLD may not become a cornerstone of our portfolio, it represents an important part of our ongoing research into alternative economies and governance models.

Liberland Dollar is more than just a token; it is a fascinating experiment in combining political ideals, territorial claims, and blockchain technology.

Sometimes the best investments are not measured only by financial return but also by the value of being part of a shared vision. With LLD, we’ve found exactly that.

Why We Launched Solana Covered Call Growth Fund

| Funds | 70 seen

On September 4, 2025, Terramatris LLC officially launched its Solana Covered Call Growth Fund, a specialized investment vehicle designed to combine the growth potential of Solana (SOL) with disciplined income generation through covered call strategies. The fund began with an initial seed investment of $100 from TerraM and a net asset value (NAV) of 1.00, setting the foundation for future expansion.

Economics Behind the Fund

The economic rationale of the fund is straightforward yet ambitious. By holding SOL tokens as the core asset, the fund is directly exposed to the appreciation potential of one of the fastest-growing blockchain ecosystems. At the same time, by systematically selling call options against these holdings, the fund generates additional yield, enhancing returns during periods of sideways or moderately bullish markets.

This dual-approach strategy allows us to:

- Capitalize on token growth while maintaining long exposure to SOL.

- Collect option premiums to generate cash flow and reduce volatility.

- Balance risk and reward in a way that reflects both traditional fund management and modern crypto-native strategies.

We classify the Solana Covered Call Growth Fund as a high-risk, high-reward investment, reflecting the volatility of digital assets combined with leveraged derivatives activity.

Fund Structure and NAV Framework

Unlike previous experimental funds at Terramatris, this initiative is structured as our first traditional private fund, operating on a private open model. NAV is calculated using widely accepted traditional investment fund methodologies, allowing investors to track performance transparently and consistently.

- NAV Launch Point: 1.00

- Structure: Private, open-ended fund

- Core Asset: Solana (SOL)

- Strategy: Long SOL exposure + covered call writing

- Investor Access: By invitation, with a minimum ticket size of $5,000

The fund is not designed for mass participation. Instead, we are positioning it as an exclusive growth product for a select circle of investors who understand both the opportunity and risks inherent in crypto markets.

Commitment and Capital Growth

While we are actively working to raise additional investment capital, Terramatris itself maintains skin in the game. Beginning September 2025 and continuing until at least September 2026, Terramatris LLC will commit to bi-weekly contributions of $100 into the fund, demonstrating confidence and alignment with investors.

For its own capital, Terramatris is employing a leveraged x2 approach, amplifying the exposure to both SOL growth and the fund’s covered call yield strategy. This ensures that the management team shares both the risks and rewards alongside external investors.

Fee Structure

The Solana Covered Call Growth Fund follows a fee model that balances sustainability with investor alignment:

- 2% annual management fee

- 20% quarterly performance fee, calculated with a high-water mark provision to ensure fees are only earned when true new performance is achieved

This structure incentivizes consistent performance while maintaining transparency and fairness for investors.

Strategic Importance for Terramatris LLC

The launch of this fund marks a critical step forward in the evolution of Terramatris LLC. It demonstrates our ability to move beyond experimental trading strategies and establish a professionally structured, traditional-style investment vehicle that can appeal to both crypto-savvy and traditional investors.

This model fund paves the way for:

- Greater institutional credibility through NAV-based valuation.

- A scalable structure for future funds with diversified strategies.

- A disciplined investor base aligned with long-term growth goals.

Our objective is to grow the fund’s value from $100 to $100,000 in a reasonable timeframe, leveraging disciplined trading, prudent risk management, and focused marketing to qualified investors.

The Solana Covered Call Growth Fund represents more than just another crypto product. It embodies our philosophy of combining innovative blockchain opportunities with sound financial structures. By blending SOL’s growth trajectory with the income potential of covered calls, we aim to deliver outsized returns to investors willing to embrace calculated risk.

This launch is not only an investment opportunity p it is a milestone in the professionalization of Terramatris LLC and a strong signal of our long-term commitment to building structured, scalable crypto investment vehicles.

Jupiter (JUP): Why This Solana DeFi Token Caught Our Attention

| Investment ideas | 43 seen

At Terramatris, we believe in allocating small portions of our portfolio to projects with meaningful upside—a strategy that led us to JUP, the governance token of Jupiter, Solana’s leading DEX aggregator.

A Surprise Airdrop: A Door to Exploration

In February 2024, we unexpectedly received JUP tokens via an airdrop in our Phantom wallet. This surprise grant sparked our curiosity. Since then, we’ve been steadily exploring Jupiter’s ecosystem—staking, voting, and observing its evolving DeFi utility—without letting excitement cloud our judgment.

What Is Jupiter—and Why It Matters

Jupiter is a decentralized exchange (DEX) aggregator on Solana, routing token swaps across over 20 liquidity sources like Raydium and Orca to find the best execution with low slippage It has grown into a core component of the Solana DeFi infrastructure, handling a significant portion of swap volume on the chain

The native token JUP serves as Jupiter's governance and utility token, enabling holders to participate in protocol decisions and earn rewards through staking and an active staking rewards (ASR) system that rewards those who vote

Real Utility—Even for TerraM Token

One feature that stands out for us is that Jupiter supports Solana-based tokens, allowing seamless swaps—which includes our own native TerraM token via the Jupiter aggregator. This enables users to trade TerraM easily within the Solana ecosystem.

Moreover, Jupiter is now entering DeFi lending with Jupiter Lend, offering borrowing and lending, including using JUP as collateral . From our perspective, the ability to borrow against TerraM on Jupiter’s platform would be a highly compelling use case.

Our JUP Position & Approach

We’ve adopted a cautious, measured approach. Our current holdings stand at just over 600 JUP tokens, acquired through staking, participating in votes, and organic accumulation. We’re aiming to grow this to around 1,000 JUP by the end of the year or in Q1 2026.

Throughout, we remain pragmatic—interested in the project’s evolving features, not overexcited. We continue to stake, vote, and engage—collecting small rewards while staying alert to how Jupiter expands into full-stack DeFi.

Our Outlook on TON: Humble Investment Today, Moonshot Tomorrow?

| Investment ideas | 26 seen

At Terramatris, we regularly allocate a small portion of our fund to assets that we believe could have asymmetric upside potential — what we call moonshots. One of those tokens today is TON (The Open Network).

Our investment in TON is currently modest: at the time of writing, we hold just under 100 TON tokens, with a possible outlook to increase this allocation to 200–300 tokens in 2026. While this is a humble position compared to our core holdings, it reflects our conviction that TON has the potential to become a significant player in the crypto ecosystem.

There are a few key reasons why we believe in TON:

1. The Pavel Durov Factor

Although Pavel Durov (the founder of Telegram and earlier, VKontakte) is not directly running TON — the project is now developed and maintained by the TON Foundation — his track record matters.

- VKontakte was inspired by global social networks, but Durov turned it into a unique platform that became Russia’s largest social media company.

- Telegram entered a competitive space of messaging apps, yet evolved into one of the most advanced, secure, and widely adopted platforms worldwide.

Durov has repeatedly shown the ability to take an idea, refine it, and push it forward into something more powerful. With TON closely tied to Telegram’s ecosystem, we believe the potential for scale is substantial.

2. TON as the Ethereum of the Telegram World

We view TON as a kind of Ethereum for Telegram. It is designed to handle millions of transactions per second, integrate seamlessly with messaging, and power a decentralized ecosystem of payments, storage, and applications.

With Telegram’s 900+ million global users, even partial adoption of TON-powered features could create strong network effects.

3. Long-Term Asymmetric Potential

Our investment philosophy here is simple: allocate small amounts to projects that could either fail or grow exponentially. We are not betting the fund on TON, but by holding a small, carefully measured position, we are exposed to its potential upside without overcommitting.

Outlook

As mentioned, our current allocation is around 100 TON tokens, with the possibility of increasing to 200–300 tokens by 2026, depending on market developments and project adoption.

We are in no rush. TON is still in its early growth phase, and we are prepared to hold for several years if needed.

This article reflects Terramatris’ internal investment decisions and is published for transparency and informational purposes only. It should not be construed as financial or investment advice. Cryptocurrencies are highly volatile, and past success of related ventures does not guarantee future performance. Each reader should do their own due diligence and consult with a licensed financial advisor before making investment decisions.

Wishful Thinking, Statistics, and Modeling: Where Could Terramatris Fund Be in September 2026?

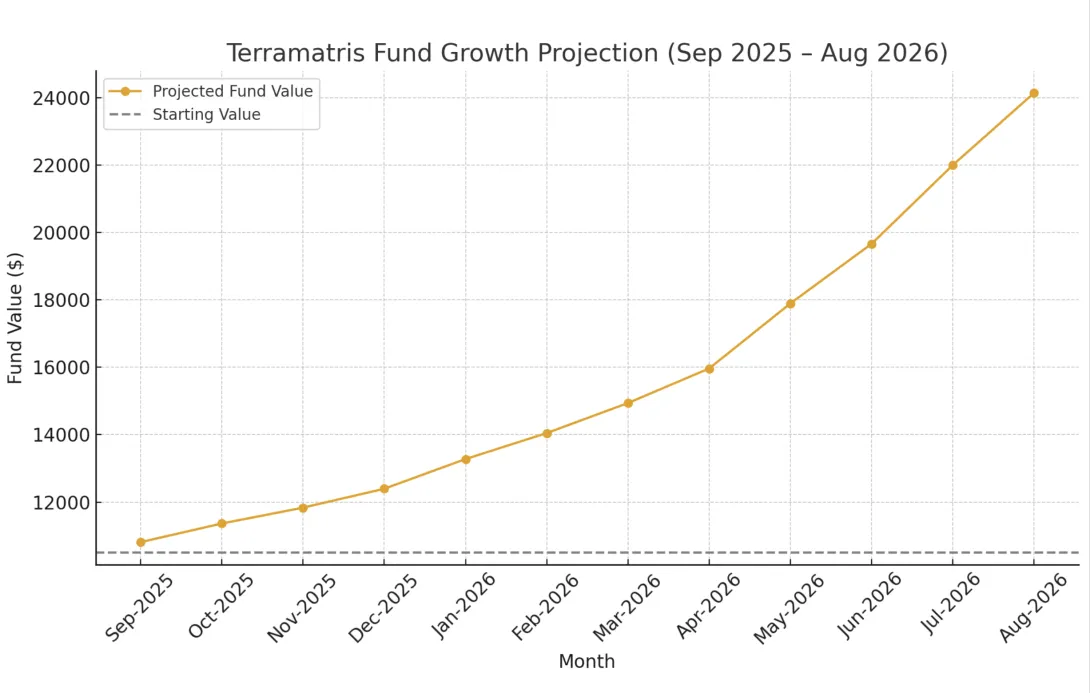

| Research | 39 seen

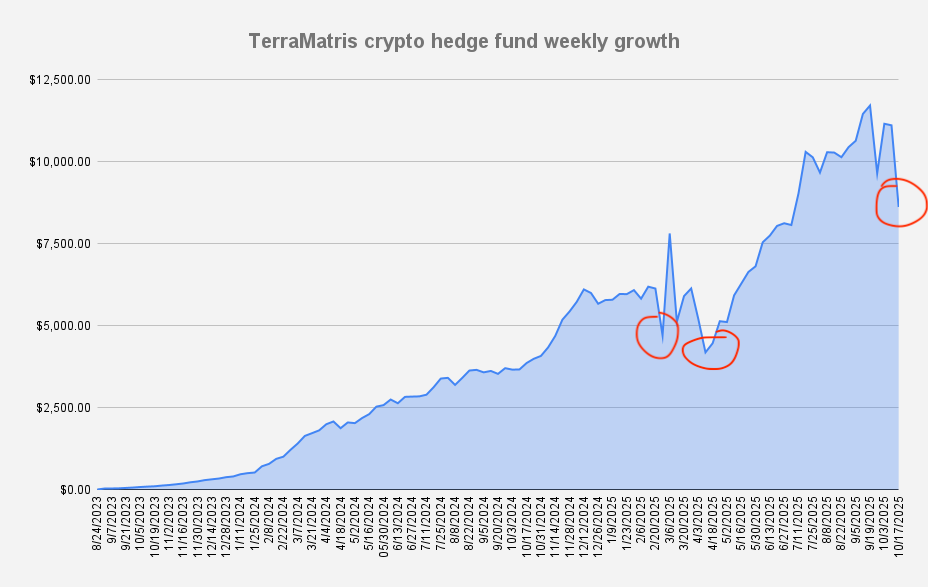

On September 2, 2025, the Terramatris crypto hedge fund stands at $10,500. Out of this, roughly $3,500 is low-interest debt, which we are steadily repaying at a rate of $300–450 per month. If nothing changes, we expect to be debt-free by April 2026. Importantly, there is no real pressure to return these funds quickly; and if market conditions turn against us, we believe we could borrow back on similar terms without risk to the core strategy.

This puts Terramatris in a comfortable position: a five-figure portfolio, a clear debt-repayment path, and a robust options premium strategy that has been delivering consistent weekly returns.

The Options Premium Engine

Our core edge comes from selling weekly options—primarily covered calls and short puts.

- Base case (regular weeks): $150 income

- High case (end-of-month weeks): $300 income

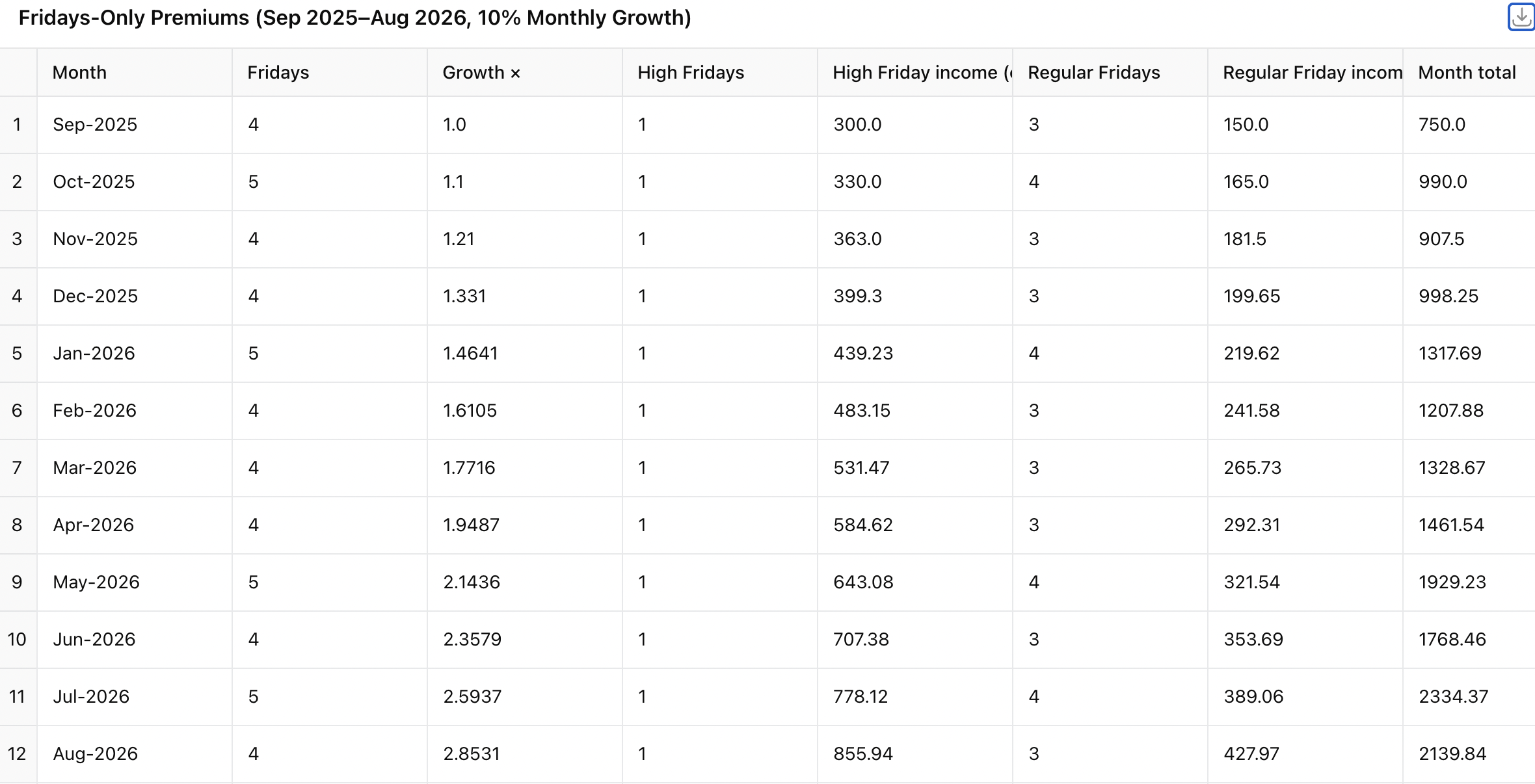

This structure mirrors what we saw in August 2025, when August 29 delivered an all-time high $580 in weekly option premium. While that was above our base projections, it demonstrates the upside potential of our systematic approach.

Statistically, this creates a 3–4 regular weeks per month followed by 1 boosted week model. The stability of this rhythm is what makes our growth projections meaningful.

Modeling Forward: A 10% Monthly Growth Scenario

For the year ahead, we assume that options income grows at 10% per month. This is a form of wishful thinking grounded in compounding mathematics:

- Start: September 2025 with $150 regular weeks, $300 high weeks

- Growth: +10% per month on both income types

- Horizon: 12 months (September 2025 – August 2026)

Using this model with the actual Friday distribution, Terramatris is projected to generate about:

- $17,133 total in options premiums from Sept 2025 → Aug 2026.

This compares to $9,600 in a linear, no-growth scenario—showing how much impact compounding can have if we keep executing consistently.

Fund Value by September 2026

Let’s combine these flows:

- Starting value (Sept 2025): $10,500

- Debt repayment by April 2026: ~($3,500) returned gradually

- Options income (1 year): +$17,133

If all premiums are reinvested and debt fully cleared by spring, the fund value in September 2026 could stand around $24,000.

That’s more than +128% growth year-over-year. Even with more conservative assumptions (say 5–6% monthly growth, or stagnant summer markets), the projection shows healthy double-digit compounding.

The TerraM Token Effect

The TerraM token is designed to reflect the performance and value of the Terramatris fund. If the fund nearly doubles in size, the token’s intrinsic backing strengthens:

- More collateral per token

- More confidence in future buybacks and liquidity

- Stronger long-term sustainability

While the crypto markets are volatile and nothing is guaranteed, a growing base fund value directly improves the TerraM token’s story. It makes the token not just a speculative asset, but a reflection of real trading income.

A Note on Wishful Thinking

All projections are based on statistics and models. Reality can diverge:

- Option premiums may dip in quiet months

- Market drawdowns may force adjustments

- Growth may not compound as neatly as modeled

That’s why we emphasize monthly reviews. Each month, we can re-test assumptions and adjust premium targets. But as a starting point, the 10% growth model provides a compelling roadmap of what’s possible.

Conclusion

By September 2026, if Terramatris executes consistently, clears its small debt, and keeps compounding weekly premiums, we could be looking at a fund size above $24,000. The journey from a $10,500 base to this level in 12 months shows how disciplined option selling and compounding growth can transform a small fund into a serious player.

Wishful thinking? Perhaps. But with math, modeling, and momentum on our side, it’s a future worth striving for.

Why We Decided to Invest in Trump Coin

| Investment ideas | 30 seen

As part of our ongoing exploration of asymmetric opportunities in the crypto markets, we have decided to make a small, opportunistic bet on Trump Coin ($TRUMP). This position will not replace or alter our core holdings in Bitcoin, Ethereum, and Solana, but will instead be structured as a side challenge using a disciplined, incremental approach.

The 52-Week Challenge

We will allocate to Trump Coin gradually over the course of one year. Starting with $1 in week one, increasing by $1 each subsequent week, and continuing through week 52, this strategy will total $1,378 in contributions if completed.

- Initial funding: Early weeks will be financed from our existing cash balances.

- Later weeks: We may allocate a portion of weekly options premiums into Trump Coin, depending on market conditions.

This structured accumulation reduces timing risk and ensures that our exposure scales modestly.

Why Trump Coin?

Unlike our core crypto holdings, Trump Coin is not optionable, meaning we cannot hedge or generate yield from covered call strategies. By adding it, we are explicitly taking opportunistic risk.

Our reasoning is simple: with President Trump in office until 2028, this token remains a powerful narrative asset tied to politics, culture, and market sentiment. The coin has already demonstrated explosive speculative potential, with a previous all-time high near $70. While there is no guarantee that history will repeat, we view a return to those levels as within the realm of possibility during this administration.

Risk Acknowledgment

We are clear that Trump Coin is not a core holding and carries significant downside risk. This allocation is strictly experimental, sized small, and designed as a side challenge rather than a pillar of our portfolio. We may be wrong in our assumptions, and the token could lose significant value.

This is not a trade recommendation, but a transparent outline of our thinking.

Closing Thought

By pursuing this 52-week Trump Coin challenge, we are adding a small but structured exposure to a unique political-meme asset. The upside is speculative, the risk is high, and the allocation is sized accordingly. Our conviction remains strongest in BTC, ETH, and SOL—but selective opportunism is part of our broader strategy.

TerraM Token Buyback and Liquidity Policy for 2025–2026

| TerraM token | 33 seen

The TerraM token derives its value from the earnings generated by the Terramatris Fund. As the fund grows, a portion of that growth is systematically directed toward strengthening token liquidity. This structure is designed to provide existing token holders with improved price stability and reduced transaction slippage.

Liquidity Management Plan

Liquidity is central to the long-term functioning of TerraM. Our structured plan includes:

- Allocation Rule: For every $1,000 in net fund growth, $200 areadded to the Raydium liquidity pool through the TerraM:USDC pair.

- Objective: Increase the pool share from the current 4.10% of tokens to 6–7% over the next growth cycle.

- Expected Impact: By expanding liquidity, we aim to reduce slippage for token holders and support a more orderly secondary market.

Buyback Policy

We are preparing a measured buyback program:

- Trigger: Buybacks will commence once at least 5% of total TerraM tokens are held in the Raydium pool.

- Price Context: As of this update, TerraM tokens trade at $3.26.

- Fund Threshold: Based on current modeling, this 5% liquidity threshold is expected once the fund’s value reaches $12,000.

- Mechanics: Buybacks will be executed directly in the market, with the primary intent of improving liquidity depth and price efficiency.

OTC Sales Policy

At present, no over-the-counter (OTC) token sales are anticipated.

- Waiting List: Any third-party interest in OTC acquisition will be placed on a list for future consideration.

- Reassessment Point: OTC discussions may resume once the fund’s value exceeds $15,000.

- Until that point, token access will remain limited to the decentralized exchange (DEX) environment.

Roadmap Toward $15,000 Fund Value

Our operational focus is directed at scaling the Terramatris Fund to $15,000 in assets under management (AUM).

- Milestone 1 – $12,000 (Expected Q4 2025)

- Initiate token buybacks upon reaching 5% pool liquidity.

- Continue 20% liquidity reinvestment policy on incremental growth.

- Milestone 2 – $13,500 (Expected early Q1 2026)

- Expand liquidity pool share toward 6–7%.

- Strengthen reserve allocations to ensure sustainable reinvestment.

- Milestone 3 – $15,000 (Target by end of Q1 2026)

- Review OTC sales framework and evaluate controlled re-entry of new investors.

- Formalize long-term liquidity strategy based on fund growth and trading volumes.

This update contains forward-looking statements regarding anticipated fund growth, liquidity management, and token policies. These statements are based on current expectations and assumptions and involve risks and uncertainties that could cause actual outcomes to differ materially. There is no guarantee that projected milestones will be achieved within the anticipated timeframe.

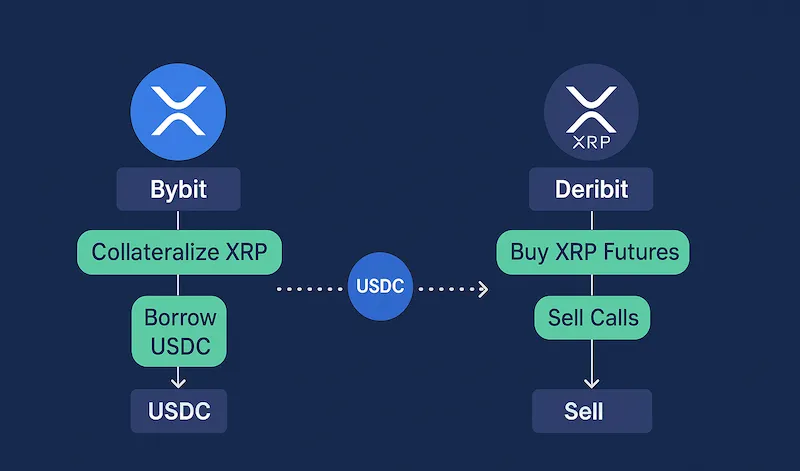

Trading Covered Calls on XRP with Deribit

| Crypto Options | 64 seen

At Terramatris we are always exploring new ways to structure option strategies around crypto assets. One of the more interesting challenges we’ve faced recently is figuring out how to trade covered calls on XRP.

Our favorite trading platform, Bybit, unfortunately does not yet offer XRP options. That left us looking for alternatives, and naturally, Deribit became our next candidate. Deribit does offer XRP options, but as always, the devil is in the details.

The Challenge: Collateral Rules on Deribit

Deribit lists XRP options, but they are settled in USDC. At the time of writing, there is no way to post XRP directly as collateral for call selling. This complicates things because in a “classic” covered call setup, you’d hold the underlying asset (XRP in this case) and sell calls against it.

Instead, Deribit requires USDC margin. That forced us to think a bit more creatively.

Our Solution: Bridging Bybit and Deribit

We came up with what we believe is a smart workaround:

- Collateralize XRP on Bybit – We locked up some of our XRP holdings on Bybit as collateral.

- Borrow USDC – Against that XRP, we borrowed USDC, paying about 11% annual interest.

- Transfer USDC to Deribit – The borrowed USDC was moved to Deribit to serve as option margin.

- Replicate XRP exposure – Since we wanted the trade to mimic a traditional covered call, we bought long XRP perpetual futures on Deribit with 25x leverage.

Effectively, this setup allowed us to hold XRP exposure (via leveraged futures) while still being able to sell call options on Deribit.

Why This Works (and Why It’s Imperfect)

This approach isn’t a perfect covered call structure, but it comes surprisingly close:

- The borrowed USDC plays the role of collateral for selling calls.

- The long XRP futures replicate holding spot XRP, giving us the underlying exposure.

- The sold calls then generate premium just like in a standard covered call strategy.

Of course, there are trade-offs:

- Borrowing USDC at 11% creates a financing cost that eats into returns.

- Using 25x leverage on the long futures introduces liquidation risk if not managed carefully.

- There is ever changing funding fee for holding perpetual futures

- It’s more complex than simply selling calls against spot XRP.

Still, as an experimental structure, it’s a viable workaround until platforms like Bybit start offering XRP options with XRP collateral support.

Looking Ahead

For us, this was a valuable exercise in thinking creatively about option structures in crypto. It’s an experiment we’ll continue to fine-tune, exploring different leverage levels, roll strategies, and ways to minimize financing costs.

The crypto options landscape is evolving quickly. For now, this setup gives us a way to monetize our XRP exposure through covered calls, even if it requires some creative bridging between platforms.

Managing Risk: Rolling Forward and Hedging With Trigger-Based Shorts

| Crypto Options | 24 seen

In the past week, one of our ETH option positions came under pressure. We were short 1.7 ETH put contracts with a 4100 strike expiring on August 22. With ETH price action weakening, the trade started to look challenged.

At Terramatris, our primary focus is risk management. Collecting option premium is attractive, but holding onto a position that feels unsafe can quickly turn into a liability. We therefore took a hard look at our choices:

- Roll forward to a later expiry to keep premium income flowing.

- Hedge with futures to neutralize delta risk.

- Combination strategies, blending both approaches.

Why It Felt Unsafe

Near-dated puts carry high gamma risk. If ETH sold off aggressively before expiry, our margin exposure would spike, forcing reactive hedging at poor prices. That is not how we operate. Instead, we prefer to anticipate the risk and structure a plan before the market forces it.

The Strategies on the Table

- Pure Roll Forward

Would maintain income, but keep us exposed to downside if ETH broke below 4100 quickly. - Pure Futures Hedge

Would cleanly offset risk, but at the cost of giving up the premium opportunity. - Partial Roll + Hedge

A balanced approach: extend part of the position for more premium while hedging the rest to protect the book.

Our Decision: Partial Roll Down and Hedge

We chose the partial roll. Specifically, we rolled a portion of the puts forward and down in strike, pushing them out to the following week. This not only maintained the position but also collected additional premium due to the skew in ETH options.

For the remainder, we implemented a trigger-based short futures hedge. This hedge activates if ETH trades into specific downside levels, automatically reducing our exposure without tying up unnecessary capital upfront.

Why This Matters

This hybrid strategy accomplishes three things:

- Preserves Income – We keep harvesting option premium.

- Manages Tail Risk – Futures hedge protects against a sharp downside move.

- Keeps Flexibility – Rolling down improves risk/reward if ETH stabilizes or rebounds.

Key Takeaway

This trade illustrates how we operate at Terramatris: never passive, always adaptive. When a position feels unsafe, we don’t sit still. We evaluate the alternatives, choose the mix that balances reward and risk, and execute decisively.

The result: a position that continues to earn, but with downside risk contained. That’s the essence of our de-worrying strategy — turning a challenged trade into a controlled one.

Snipping in DeFi: Tempting, But Not Sustainable

| Research | 47 seen

At Terramatris, we constantly evaluate emerging strategies in the decentralized finance (DeFi) landscape — especially those that promise asymmetric upside. One such tactic is snipping (or sniping), a method that’s gained attention for its high-speed, high-risk approach to token trading.

We want to offer a clear and honest take: while snipping can be entertaining and, in rare cases, wildly profitable, it doesn’t align with our long-term trading philosophy.

What Is Snipping in DeFi?

Snipping refers to the practice of purchasing newly launched tokens at the exact moment liquidity is added to decentralized exchanges (DEXs) like Uniswap or Raydium. Traders — typically using bots — aim to front-run others by getting in before a price surge and exiting moments later with a quick profit.

Snipping usually involves:

- Monitoring new token pair creations.

- Using bots or scripts to submit early, pre-signed transactions.

- Bidding higher gas prices to outpace competitors.

Our Exploration: Interesting, but Not Convincing

To be clear — we have not run any snipping bots ourselves, nor have we deployed capital into active sniping strategies.

However, we’ve explored several publicly available bots, platforms, and tactics. We’ve analyzed codebases, reviewed community feedback, and simulated edge-case scenarios.

Our conclusion?

It’s more fun than it is sustainable.

Snipping appears built for adrenaline, not for stable growth. The field is littered with failed attempts, honeypots, blacklisted contracts, and high gas loss ratios.

It’s difficult to repeat. Impossible to scale. And often too dangerous to justify.

Raydium, Solana & Our Token

Our own Terramatris Token (TERRAM) is live on the Solana blockchain, and available for trading on the Raydium Automated Market Maker (AMM).

Raydium has recently gained significant popularity as the go-to platform for launching new Solana-based tokens — largely because of ultra-low transaction fees and a frictionless developer experience. These advantages have also made Raydium a hotspot for sniping bots, especially during new token launches.

Why We’re Not Betting on It

While we don’t discount the possibility that some early snipers made big returns — especially in the initial DeFi waves — we see too many red flags to consider it a long-term, fund-worthy strategy.