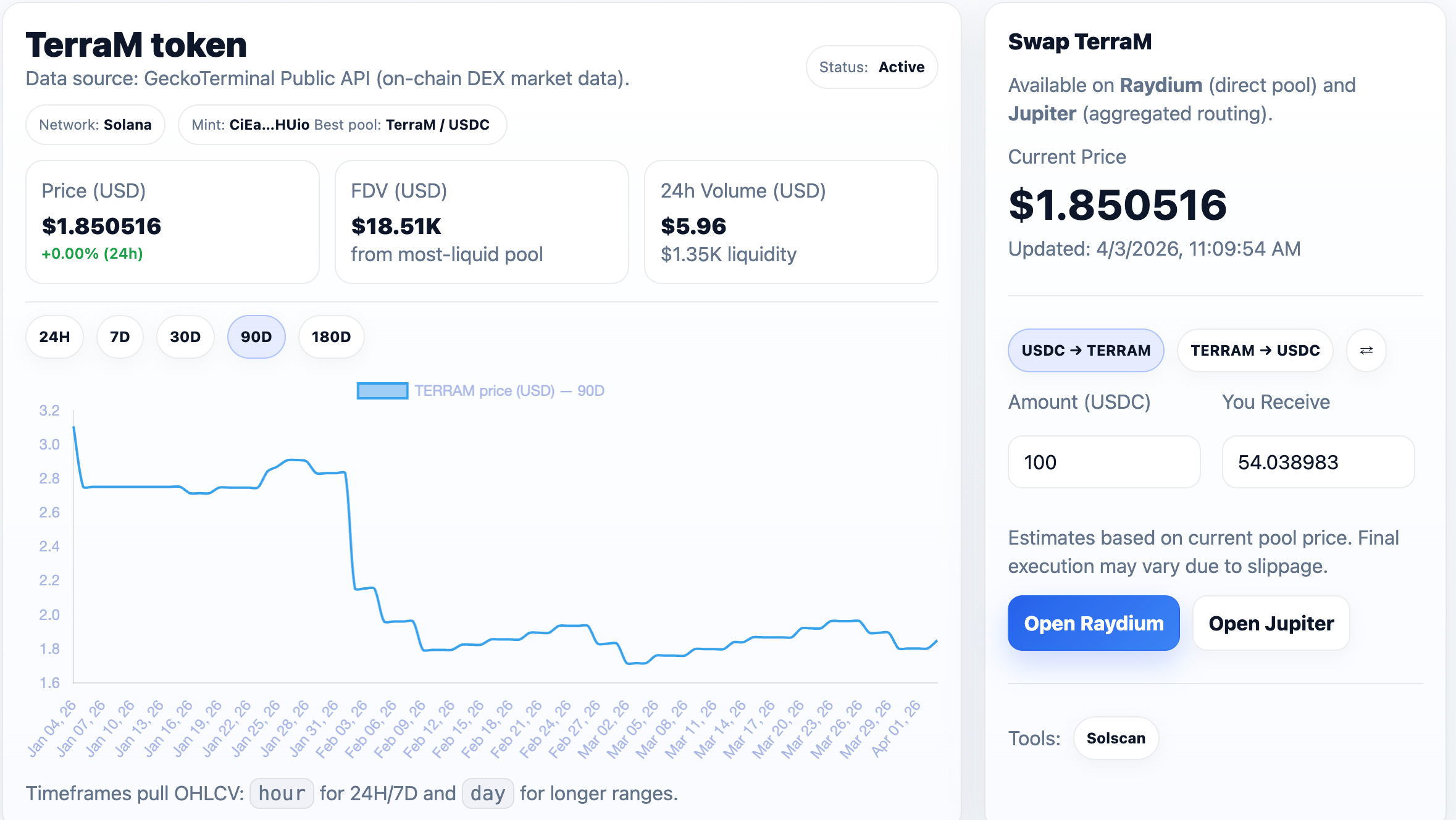

On April 3, 2026, the TerraM token traded at $1.85, down -8.4% week over week. On-chain activity was limited during the period, with two buys and one sell. The sell order pushed the price down but also increased pool liquidity; with a small buyback, we were able to stabilize the token.

During the week total TerraM liquidity on the Raydium pool increased to 3.63% of total supply.

Our broader objective remains to expand liquidity coverage to 10%, with a near-term milestone of reaching 4%. With continued buybacks in place, we expect TerraM to reach the $2–$2.2 range by the end of month, though some volatility should be expected.

Until liquidity deepens further, elevated slippage should be expected.

Ethereum strategy

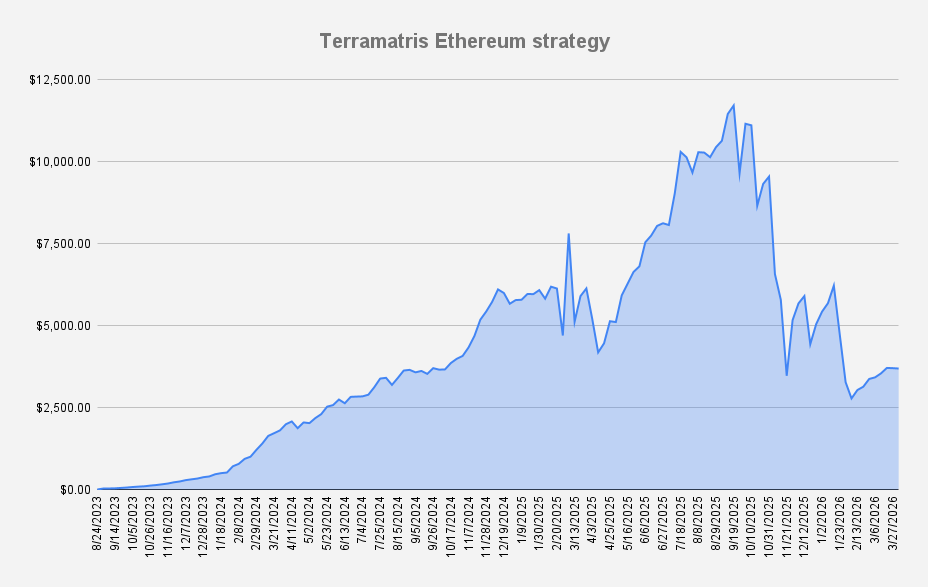

Week over week, the Ethereum strategy dipped -0.29%. This has been a solid week for ETH overall. At one point, it traded around $2,100 before easing to $2,050 closer to the weekend, aligning well with our covered call strikes. This allowed us to roll positions forward at more favorable premiums.

From the all-time high in September 2025, the fund is still down -68.47%. While YTD performance stands at -31.38%, just slightly underperforming ETH itself, which is down -30.19% over the same period.

Our short-term goal is to return the strategy to positive YTD performance; from there, the focus shifts to recovering and ultimately surpassing previous all-time highs. In an ideal scenario, the strategy should also outperform ETH itself.

During the week, the ETH Strategy generated $119 in options premiums, reducing our effective ETH break-even price to $1,474. By week’s end, the strategy held 2.05678 ETH with an average acquisition price of $1,983.

This week, we decided to reinvest part of the premium into spot ETH to benefit from a potential price recovery. Over the past two months, we have not been accumulating spot ETH, focusing instead on reducing debt.

For April, the plan is to gradually increase our spot position while keeping margin risk under control.

Current options positions:

- 1.6 ETH APR 10, 2026 2,050 Covered Call

- 0.4 ETH APR 10, 2026 2,100 Covered Call

We rolled last week’s $2,050 covered call forward to next Friday, maintaining the same strike. With ETH trading around $2,060, this caps our upside, which we are fully comfortable with. Besides that we managed laddering our covered calls, having sold a smaller portion at a higher $2,100 strike.

Additionally, we eliminated tail risk by avoiding further put selling, which gives us more flexibility to maneuver going forward.

From the options premium received, we reduced margin debt to –$1,440. The immediate objective is to bring margin back to zero without selling any ETH.

At an average premium of $119 per week, it would take approximately 12 weeks to eliminate the remaining margin balance — around end of June.

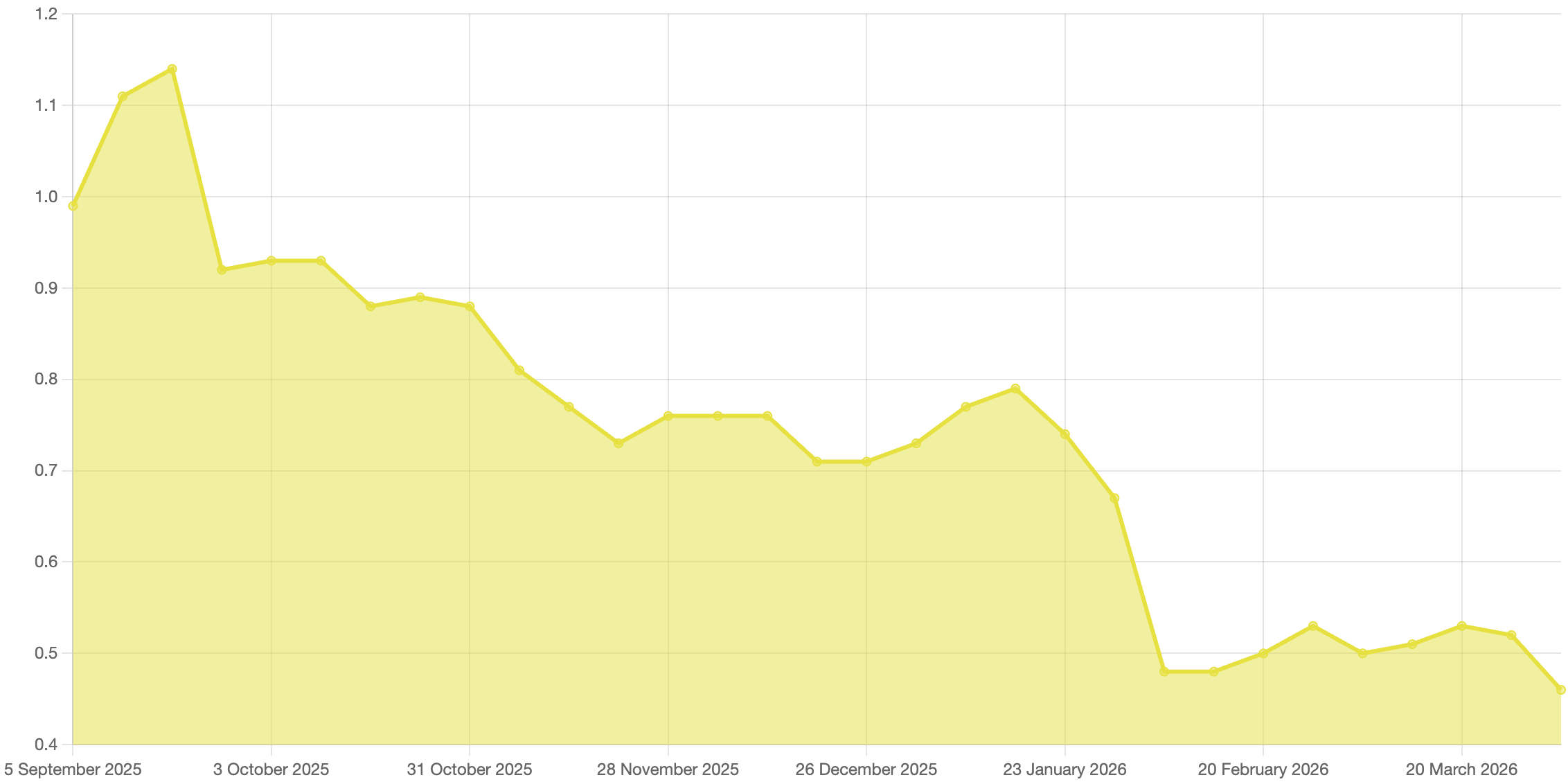

Solana Strategy

The Solana strategy took a larger hit this week: -11.34% WoW, with NAV down to $0.46. Solana fell below $80, pushing an already difficult position deeper underwater.

By the end of the week, we increased our long spot position to 57.80 SOL, with a buy price at $157.02 and break-even price of $140.16. With Solana trading at $79.96 at the time of writing, the position is significantly underwater.

During the week, we collected $16.07 in option premium by selling covered calls expiring on April 10 and May 29.

Because the position is currently underwater, our flexibility is limited. To generate meaningful premium, we had to sell calls below our average entry price, effectively capping part of the upside recovery.

Overall our Solana Strategy YTD performance is -38.37%, just slightly outperforming SOL itself, which is down -35.81% over the same period.

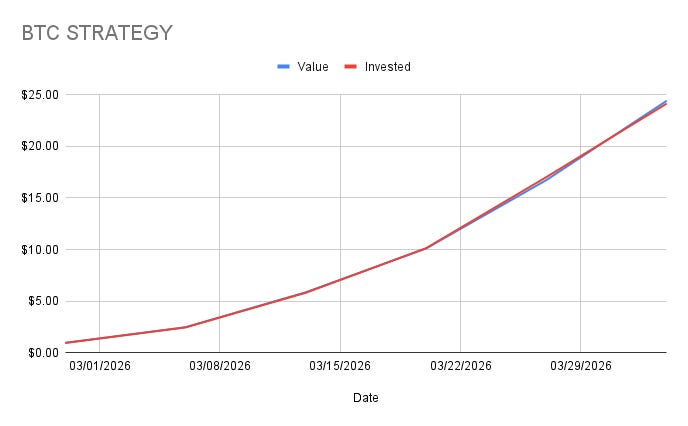

Bitcoin Strategy

This week we allocated 6% of the total options income from the Ethereum strategy to purchase spot BTC, increasing our holdings to 0.00034978 BTC

It will take several months before this position becomes noticeable, but we like the start. After five week since the launch our Bitcoin strategy is down -4.16%, Given the fund’s size, the impact is negligible.

Bottom line

TerraM remains liquidity-constrained but stabilizing, with incremental buybacks supporting price while targeting 4% pool depth near term.

The Ethereum strategy is holding relatively well versus ETH, generating steady premium income and progressing toward margin neutrality, though still deeply below ATH. Solana remains the weakest segment with limited flexibility and significant unrealized losses. Bitcoin exposure is small but steadily accumulating.

Overall, the fund is in a recovery phase—prioritizing debt reduction, liquidity growth, and gradual spot accumulation while accepting short-term volatility.