As of June 19, 2026, our Ethereum strategy portfolio was valued at $3,116, down 42.15% year-to-date. While that number is never pleasant to see, periods like this are part of investing in both crypto and options.

Rather than chasing risky trades to recover losses quickly, we continue to focus on a disciplined strategy built around generating option premium, managing risk, and gradually lowering our effective cost basis.

Compared with Ethereum itself, the portfolio has performed almost identically, with ETH down approximately 41.54% over the same period. In other words, the portfolio has largely tracked its core underlying asset while continuing to generate option premium along the way.

For readers new to this strategy, start with How to Generate Income With Ethereum Options.

Ethereum Covered Call Position

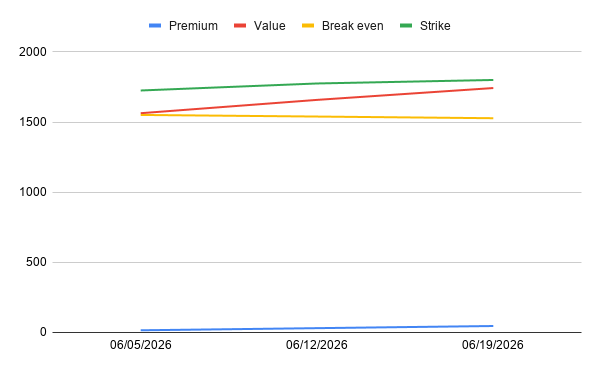

This week, we managed 1.3 Ethereum covered calls while holding approximately 1.28 ETH in the portfolio.

Our average purchase price is $1,563 per ETH, but thanks to option premiums collected over recent months, our effective cost basis has already been reduced to approximately $1,527 per ETH.

Put simply, every covered call sold has helped lower the Ethereum price we need in order to break even. While the market remains volatile, the strategy continues to do what it was designed to do: generate income, improve our position over time, and keep us invested in Ethereum for the long term.

Learn more: How to Generate Income With Ethereum Covered Calls.

Rolling the Covered Call Forward and Up

During the week, Ethereum traded in a relatively wide range between $1,720 and $1,830. As ETH approached the $1,800 level, I decided to proactively manage our covered call position rather than wait until expiration.

Specifically, I bought back our existing $1,775 covered call and rolled the position forward by selling next week's $1,800 covered call.

The adjustment generated an additional $15.30 in premium income while also increasing our potential sale price by $25 per ETH.

This is the kind of roll I like: it generated a credit, raised the strike, and kept the strategy active without adding leverage or requiring additional capital.

For a deeper explanation of this decision-making process, see When to Roll Ethereum Covered Calls.

Current Position

- 1.3 ETH Jun 26, 2026 $1,800 covered call

If Ethereum continues higher and gets called away at $1,800, we would realize a strong profit on the underlying position in addition to all premiums collected along the way.

If ETH remains below the new strike, we keep the premium, continue holding the asset, and can evaluate another covered call sale next week.

Potential Outcome if Assigned at $1,800

If our position is called away next week at the $1,800 strike price, the trade would generate a total profit of approximately $367, representing a return of 23.53% in just 21 days.

On a simple annualized basis, that equates to roughly 400% per year, although such returns should not be expected consistently over long periods.

This would be a highly welcome outcome.

Under our current policy, 50% of the realized profit would be allocated toward TerraM token support and buybacks. Given the recent weakness in the TerraM token price, such a contribution could provide a meaningful boost to the ecosystem while rewarding long-term holders.

If Ethereum does not reach the $1,800 strike price, no profit distribution will occur. Instead, we will continue selling weekly covered calls against the position, collecting additional premium and gradually lowering our effective break-even price.

What Happens After Assignment?

If the position is eventually called away, our plan would be to redeploy capital using either cash-secured puts or credit spreads.

This follows the basic logic of the Wheel Strategy: sell puts to potentially re-enter Ethereum at attractive prices, then sell covered calls once the asset is back in the portfolio.

Learn more:

- How to Generate Income With Ethereum Cash-Secured Puts

- How to Generate Income With Ethereum Credit Spreads

No Leverage, No Margin

We are not using leverage or margin at the moment, and we hope to keep it that way.

The trade-off is simple: without leverage, both gains and losses tend to accumulate more slowly. That may sound less exciting, but in investing, boring is often a good thing. Exciting usually means higher risk, larger drawdowns, and more opportunities to make costly mistakes.

One of our medium-term goals is to grow the portfolio back to its previous all-time high of $11,719, reached in September 2025.

Getting there will not happen overnight. At the current pace of collecting roughly $15 per week in option premium, it would take a very long time to close that gap through premiums alone.

That said, the strategy is not built around chasing unrealistic returns. Every premium collected lowers our cost basis, increases available capital, and creates opportunities to compound over time.

Combined with favorable market conditions and disciplined position management, we believe this approach gives us the best chance of steadily rebuilding the portfolio while keeping risk under control.

For now, we are comfortable with slow and steady progress.

Final Thoughts

This week was a useful reminder that covered call management is not about predicting every move in Ethereum.

It is about making reasonable adjustments when the opportunity appears, collecting premium when the market offers it, and staying disciplined through both drawdowns and recoveries.

Rolling the covered call from $1,775 to $1,800 for a credit improved the position and kept the wheel strategy active for another week.

If ETH is called away, we will treat it as a successful completed trade. If not, we will continue collecting premium and lowering our break-even price.

Either outcome is acceptable.

Continue Learning

Join the OptionsBrew newsletter

Get practical notes on options income, trade adjustments, and risk management.