Despite one of the weakest premium-selling weeks (#144) in months, the fund made one of its most important strategic transitions yet: moving toward a margin-free structure while continuing to accumulate long-term ETH and SOL exposure during a deeply unfavorable market environment.

Ethereum short puts moved into the money as ETH briefly fell below $2,130, forcing a series of active position management decisions involving rolls, assignments, perpetual futures, and covered calls. At the same time, the fund secured additional liquidity through an internal 0% interest loan, allowing us to fully eliminate brokerage margin debt without reducing core ETH holdings.

Meanwhile, the Solana strategy remained heavily underwater, but instead of capping upside through aggressive covered call selling, we continued averaging down and shifted focus toward staking and long-term accumulation.

On the TerraM side, buybacks were temporarily paused as we redirected capital toward strengthening Raydium liquidity — a decision aimed at improving long-term token stability rather than pursuing short-term price support.

The result is a noticeably more conservative portfolio structure, lower leverage, and reduced weekly premium generation — intentionally sacrificing short-term excitement in favor of survival, stability, and long-term compounding.

Ethereum strategy

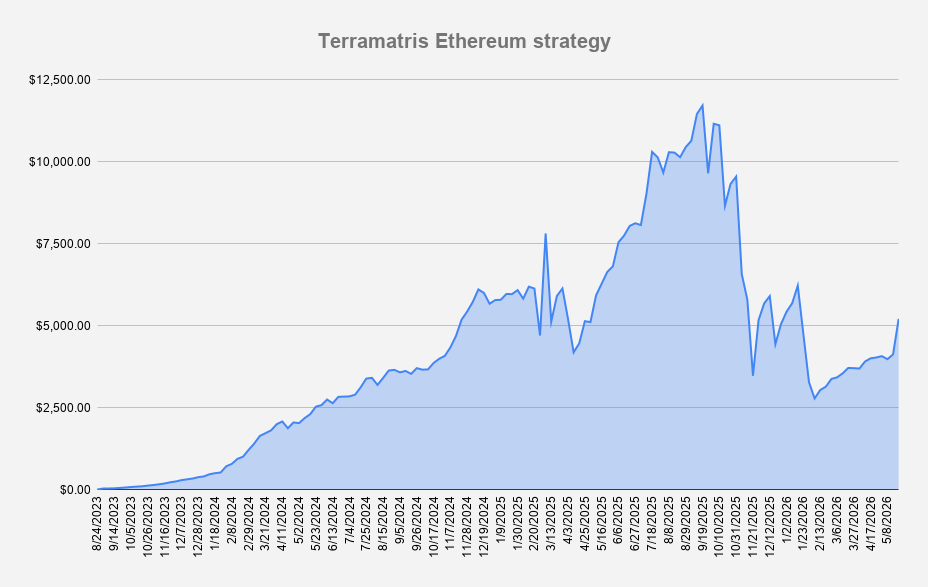

On a weekly basis, the Ethereum strategy delivered a return of 26.31%. This growth was driven by an internal 0% interest loan, which will be repaid over the coming months using weekly options premium income. We chose to use the loan proceeds to fully close our brokerage margin debt and transition toward margin-free trading going forward. While we could have sold part of our ETH holdings to reduce exposure, we decided against it due to our long-term conviction in Ethereum.

Unfortunately, this was not a strong week for premium selling.

Our $2,250 short puts moved deep in the money, and we adopted a laddered approach to manage the position. We rolled 2 ETH worth of contracts to next week’s expiry at the same strike price, while accepting assignment on 0.1 ETH. To manage the assigned position, we used long perpetual futures and sold covered calls against them with a June 26, 2026 expiry and a $2,500 strike price.

From the all-time high in September 2025, the fund is still down -55.54%. While YTD performance currently stands at -3.23%, the fund is outperforming ETH itself, which is down -28.39% over the same period.

That said, the comparison is somewhat distorted by the fresh capital injected into the fund. Since this capital effectively functions as a temporary loan, and we expect to repay it during 2026, we still consider the comparison against ETH relevant for evaluating underlying strategy performance.

During the week, the ETH Strategy generated $9.09 in options premium income. By the end of the week, the strategy held 1.74 ETH with an average acquisition price of $1,989.

This was one of the weakest premium-generating weeks we have seen in months - levels not observed since the early days of the fund. It was back in 2023 when we last earned $9 per week.

Nevertheless, our focus remains on preserving and managing positions responsibly rather than taking unnecessary risks or engaging in speculative trading.

We expect weekly options premium income to remain in the low double digits for the foreseeable future, as we are intentionally scaling back leverage and reducing overall trade aggressiveness. At this stage, we would rather target a steady +20% annual return than pursue 100% gains followed by 200% drawdowns.

Our focus is shifting toward long-term accumulation while systematically selling weekly delta 0.15 put and call options. In the event of a strong market recovery, we currently view ETH at $5,000 as a reasonable take-profit or partial exit level.

The fund strategy is becoming more conservative — and that is intentional. Boring is good.

Current options positions:

- 2 ETH MAY 29 2026 2250 Cash-Secured Put

- 1.5 ETH MAY 29, 2026 2,100 Covered Call

- 0.1 ETH MAY 29, 2026 2,200 Covered Call

- 0.1 ETH MAY 29, 2026 2,400 Covered Call

- 0.1 ETH JUN 29, 2026 2500 Covered Call (backed by long perpetual futures)

- 0.4 ETH JUN 29, 2026 2,100 Cash-Secured Put

- 0.1 ETH JUL 31, 2026 2,100 Cash-Secured Put

This week, we were holding 2.2 ETH short put positions with a strike price of $2,250. As Ethereum briefly dipped below $2,130, the positions moved into the money — not severely, but enough to require active management decisions.

Several scenarios were considered, including taking assignment, transitioning into covered calls, or rolling positions forward. In the end, we decided to combine all three approaches as part of a flexible risk management strategy.

The majority of the exposure — 2 ETH contracts — was rolled forward to the following week while maintaining the same $2,250 strike price, allowing us to collect additional premium while preserving the original thesis.

Additionally, 0.1 ETH was rolled both lower and further out in time, to the July 31 expiry with a reduced $2,100 strike price. Given current market conditions, we view this adjustment as a reasonable and constructive outcome.

We also decided to take assignment on 0.1 ETH exposure through a long perpetual futures position rather than spot crypto. Against this position, we sold a June 26 expiry covered call. Separately, we purchased 0.1 ETH at the effective $2,250 assignment level and sold a June 26 covered call with a $2,500 strike price for additional premium income.

When selecting the covered call strike, we intentionally targeted an approximate delta of 0.15. This approach leaves room for upside recovery while making future roll-up and roll-forward adjustments easier in the event of a stronger market rebound.

Finally, the remaining 2 ETH short put exposure was rolled to next week’s expiry while retaining the original strike price.

Solana Strategy

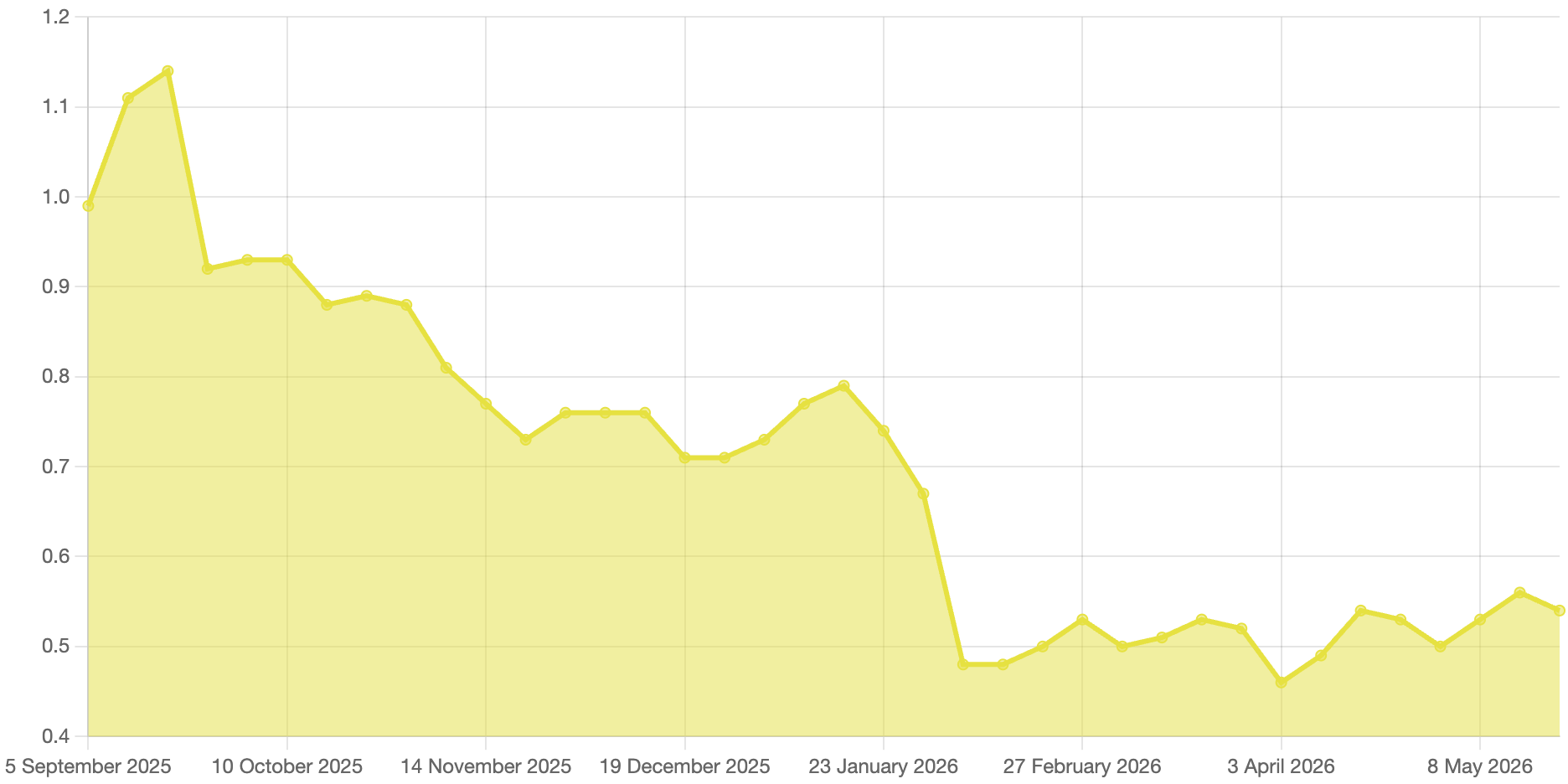

After few weeks of growth our Solana strategy decreased this week by -4.26%. NAV per unit decreased to $0.54, while SOL was trading at approximately $86.73 per token.

By the end of the week, we increased our long spot position to 67.07 SOL, with a buy price at $166.19 and break-even price of $143.84. With Solana trading at $86 at the time of writing, the position is significantly underwater.

This week, we did not sell any options, resulting in zero options income.

As our current positions remain significantly below both purchase and break-even levels, we continued increasing our SOL exposure through dollar-cost averaging. However, we deliberately avoided selling covered calls against newly accumulated SOL in order to preserve full upside potential during a possible market recovery. Instead, these holdings are being utilized for staking activities. This week, 5 SOL were staked via bbSOL, generating an estimated annual yield of approximately 5%.

Solana Strategy YTD performance is -27.21%, slightly outperforming SOL itself, which is down -30.39% over the same period.

TerraM token

On May 22, 2026, the TerraM token traded at $2.22, up 0% change week over week. There were no on-chain activity,

25% of this week’s options income was allocated toward strengthening liquidity in the Raydium AMM pool (TerraM:USDC), increasing pool liquidity to 4.66% of the total TerraM token circulation.

At this stage, we have decided to temporarily pause token buybacks until liquidity reaches at least 6% of circulating supply. As a result, the full 25% allocation will continue to be directed toward liquidity provision rather than repurchases.

Despite this adjustment in capital allocation, our short-term TerraM price target of $2.50 remains reasonable and unchanged.

Whats next?

Next week promises to be quite active, with a large number of options expiries across all of our strategies.

Within the Ethereum strategy, we will need to actively manage 2 ETH short put positions alongside 1.7 ETH worth of covered calls. At the same time, the Solana strategy will require management of 67 SOL covered calls, most of which are expected to be rolled forward to the June 26 expiry cycle.

Much will depend on overall market conditions and volatility during the week ahead. If crypto markets continue stabilizing or recover further, we may gradually roll positions higher and further out in time. Conversely, if weakness persists, our focus will remain on defensive positioning, disciplined premium collection, and controlled accumulation.

Join the OptionsBrew newsletter

Get practical notes on options income, trade adjustments, and risk management.