Welcome to another hectic week (#146) in digital assets.

Last week was yet another brutal one for crypto traders, including options sellers. With Ethereum dipping under $1,700 without any obvious fundamental catalyst (except bitcoin selloff), reinforcing a lesson we’ve learned many times before: crypto markets should not always be approached through a traditional valuation lens. Price action is often driven less by fundamentals and more by volatility, leverage, liquidity, and positioning.

What we witnessed last week appears to have been a significant leverage washout, which doesn’t come as a surprise. In last week’s update, we already highlighted the possibility of a forced deleveraging event, and that seems to be exactly what played out.

We are not excluding the possibility of another flash selloff - potentially accompanied by increased volume and aggressive short positioning - pushing ETH down toward the $1,800–1,750 range before any meaningful recovery takes place.

The question now is whether the worst is behind us or if more pain lies ahead.

From a technical perspective, many indicators suggest that the market is approaching, or may have already reached, a local bottom. Sentiment has deteriorated sharply, leveraged positions have been flushed out, and several key support zones are being tested. While further downside cannot be ruled out, the probability of stabilization and a relief rally is increasing.

As always in crypto, certainty is impossible. But if the recent move was primarily driven by leverage rather than a meaningful deterioration in fundamentals, the conditions for a bottom are beginning to emerge. The question is whether this is the absolute bottom, or just a bottom before the next leg down.

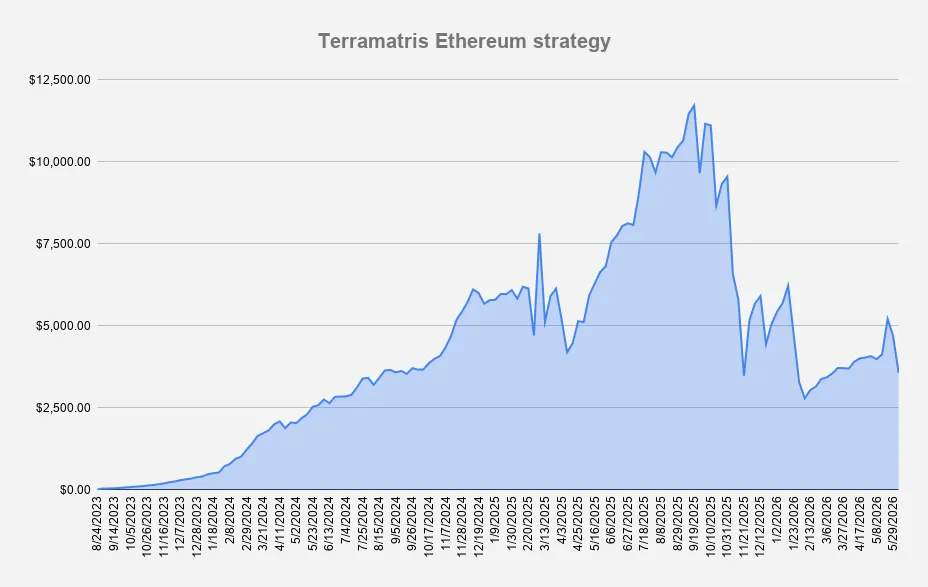

Ethereum Strategy

On a weekly basis, the Ethereum strategy decreased by -23.94%. Our loan position added last week has now been completely wiped out.

The question we should be asking today is: would we be down 50% this week without the loan, or would we still be down only 23%?

Last week, we faced a difficult choice: either close our long positions and avoid taking on additional debt, or take a loan and keep those positions open. In the short term, closing the positions would have been the smarter decision. Whether that would have been the better long-term decision remains uncertain.

If there is one lesson from this experience, it is that loans and margin are rarely your friends in crypto. They can amplify gains, but they also magnify losses and reduce your ability to survive periods of extreme volatility.

The steep decline has been driven by both the drop in our long holdings and additional pressure from our 1.6 short ETH $2,300 put options expiring at the end of June.

Tail risk remains significant. With ETH trading at $1,682 at the time of writing, our short put position is showing an unrealized loss of approximately $988. As ETH continues to move further below the strike price, rolling the position forward becomes increasingly difficult and expensive.

While the current losses remain unrealized, the position highlights the risks of selling puts in highly volatile markets, especially when combined with leverage elsewhere in the portfolio.

In an ideal scenario, ETH would trade above $2,300 by the end of June, allowing us to fully offset the current losses. Otherwise, we will likely continue rolling positions forward and harvesting option premiums while managing overall exposure and capital at risk

From the all-time high in September 2025, the fund is down -69.57%. While YTD performance currently stands at -33.78%, the fund is outperforming ETH itself, which is down -43.35% over the same period.

During the week, the ETH Strategy generated $50.16 in options premium income. By the end of the week, the strategy held 1.76 ETH with an average acquisition price of $2,001. while the break even price is much more better: $1,066. I

n the event that we are assigned on our 1.6 ETH short puts at the $2,300 strike price, our average break-even price would increase to approximately $1,621. While this would raise our cost basis, it would still technically leave us with a small overall gain relative to the market decline that began in early February.

In other words, despite the current drawdown, the position would remain slightly profitable as long as ETH holds above our adjusted break-even level.

Current options positions:

- 1.7 ETH JUN 12, 2026 1,950 Covered Call

- 0.1 ETH JUN 26, 2026 2500 Covered Call (backed by long perpetual futures)

- 0.1 ETH JUN 26, 2026 2300 Covered Call (backed by long perpetual futures)

- 1.6 ETH JUN 26, 2026 2,300 Cash-Secured Put

- 0.1 ETH JUL 31, 2026 2,100 Cash-Secured Put

- 0.4 ETH MAR 26, 2026 1,800 Cash-Secured Put

Before the major flash crash, we managed to roll 0.4 ETH put options from a $2,100 strike with a June-end expiration to a March 26, 2027 expiration, while also reducing the strike price to $1,800.

This adjustment provided additional downside protection and significantly extended the time available for the position to recover. While the roll came at the cost of locking in the position for a much longer period, it reduced our immediate assignment risk and lowered our effective purchase price if assignment eventually occurs.

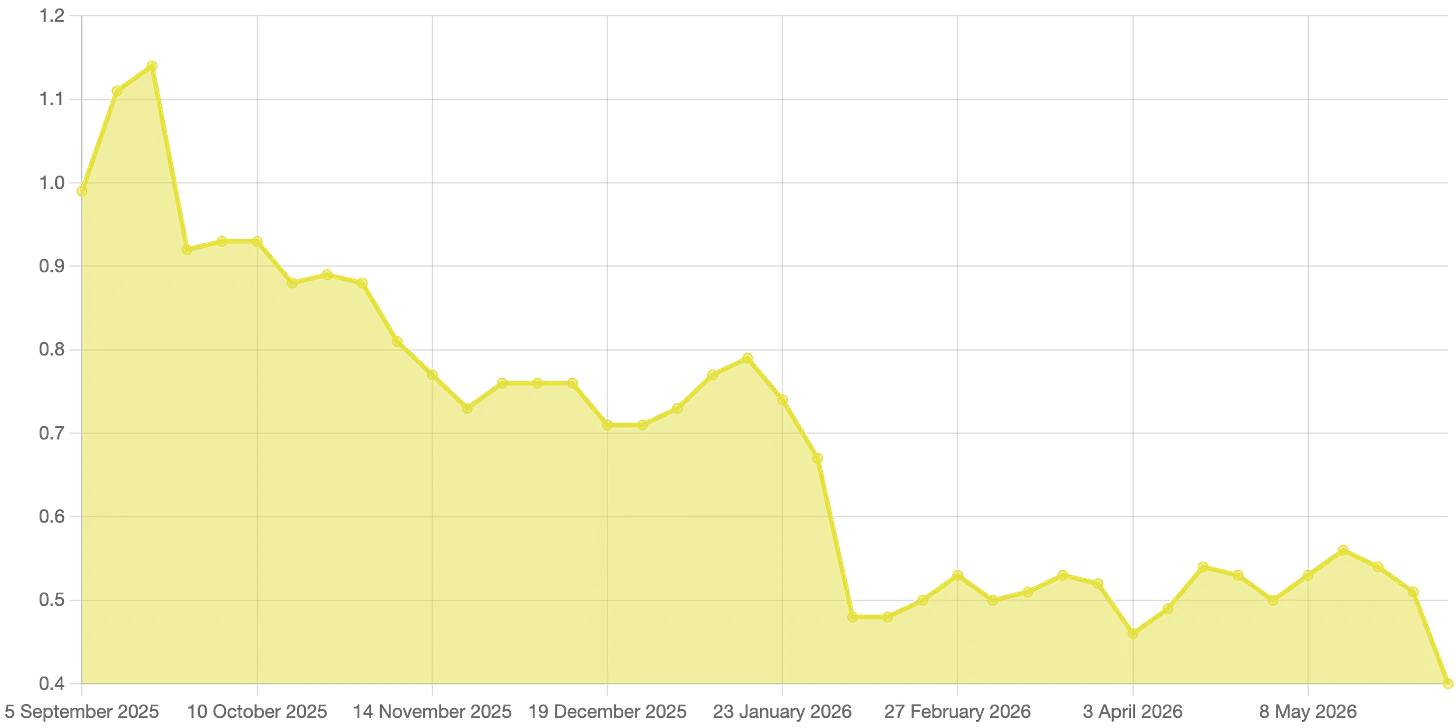

Solana Strategy

Solana strategy was not saved either and decreased by another -22.07%. NAV per unit decreased to $0.40, while SOL was trading at approximately $64 per token.

By the end of the week, we increased our long spot position to 71.07 SOL, with a buy price at $163.69 and break-even price of $141.54. With Solana trading at $64 at the time of writing, the position is significantly underwater.

During the week, we did not collect any options premium. Instead, we added 4 SOL to our staking position.

Given how deeply underwater our portfolio currently is, we do not want to cap potential upside by selling covered calls or taking on additional short-option exposure at current levels. If a recovery materializes, we want to participate as fully as possible.

In the meantime, we are relying on staking to generate yield. While the returns are relatively modest, staking provides a steady source of passive income without limiting upside potential or adding further risk to the portfolio.

Solana Strategy YTD performance is -46.23%, slightly outperforming SOL itself, which is down 48.02% over the same period.

TerraM token

On May 29, 2026, the TerraM token traded at $2.11, down - 5.21% week over week. There was one on-chain sell transaction during the week, which temporarily pushed the token price lower. However, it also increased the liquidity ratio to 5.35%.

Due to the sharp market selloff and the significant drawdown in the ETH Fund, we made the short-term decision not to distribute 50% of this week’s premium to the Raydium liquidity pool. Instead, we retained those funds within the portfolio to strengthen our position during this period of elevated volatility.

This should be viewed as an extraordinary measure rather than a change in policy. Assuming the fund generates option premium next week, we intend to resume adding liquidity to the pool. We also plan to restart token buybacks once the liquidity ratio reaches 6%.

Our priority at the moment is preserving capital and maintaining flexibility while navigating the current market conditions.

What Next?

The events of the past week have reinforced a simple truth: survival comes first.

While the drawdowns have been painful, both the ETH and SOL strategies remain operational, continue to generate yield, and maintain exposure to any eventual market recovery. Our primary focus in the coming weeks will be risk management, capital preservation, and gradually improving portfolio positioning rather than aggressively pursuing returns.

For the ETH strategy, much will depend on whether Ethereum can stabilize above current levels. A move back above $2,000 would significantly improve our ability to manage and roll existing short put exposure. Conversely, another wave of forced selling could create additional challenges, particularly for our June expirations.

The Solana strategy is currently focused on patience. Rather than selling upside through covered calls at depressed prices, we are prioritizing spot accumulation and staking rewards while waiting for market conditions to improve.

At the fund level, we expect volatility to remain elevated. Markets rarely move in a straight line after major deleveraging events. Even if a bottom has formed, sharp rallies and equally sharp pullbacks should be expected.

Looking ahead, our objectives are straightforward:

- Continue generating option premium where risk-reward remains attractive.

- Avoid excessive leverage and margin exposure.

- Maintain sufficient liquidity to navigate further volatility.

- Gradually rebuild NAV through disciplined position management.

- Resume liquidity additions and TerraM buybacks once portfolio conditions allow.

The coming weeks will likely determine whether this was the final capitulation of the cycle or merely another step in a longer correction. Either way, our focus remains unchanged: stay solvent, stay disciplined, and stay positioned for the eventual recovery.